UAE: survival of the fittest

The property and construction sector slowdown continues to impact on UAE cement producers, driving utilisation levels and prices down when production capacity has increased to over 40Mt – well in excess of the 12Mta market demand. Lately, margins have been further squeezed as operating costs rise. Meanwhile, rumours abound that various plants have been put up for sale, perhaps signalling a turning point for this beleaguered market.

The UAE‘s cement sector has experienced some of the most dramatic changes in recent years as boom has turned to bust in the construction sector. A decade ago, demand was just 6.4Mta, equivalent to 1911kg per capita – typical of the rapidly-expanding GCC markets. By 2008, demand had skyrocketed, raising per capita consumption to 4365kg at its peak.

Indeed, as the decade progressed, business sentiment grew stronger with each passing year as oil prices climbed and the UAE became the centre of a regional construction boom, epitomised by the audacious real estate mega-developments in Dubai, such as the Nakheel Palms and the Burj Khalifa.

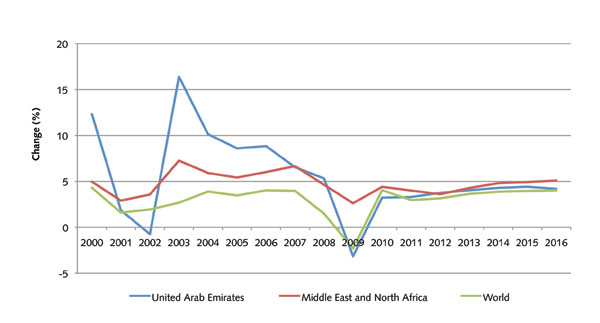

Figure 1: GDP growth vs MENA and world

The economy surged, significantly outperforming the MENA and average world GDP growth rates (see Figure 1). In terms of cement consumption, the UAE saw even higher rates of growth, with CAGR for 2003-08 reaching an impressive 25 per cent. Growth appeared inevitable and unstoppable. Cement producers were able to demand high prices as the rapidly-expanding market was undersupplied. Profits margins escalated, and investors with easily-available credit were drawn in their hoards to the industry, eager to set up a new plant and print money.

In less than 10 years, the size of the UAE’s cement industry quadrupled, adding some 30Mt of new cement capacity. Today, there are 22 production facilities, including two 10,000tpd lines, at Union Cement Company and Arkan, plus 11 grinding plants and one dedicated clinker plant. Domestic clinker capacity now stands at 26.9Mta, up from 10.4Mta in 2003, while cement capacity has reached 40.5Mta (an equivalent supply of 7316kg per capita). Dedicated grinding capacity is calculated at 12.4Mta.