China: ready for a new era?

The 13th China International Cement Industry Exhibition and Cement Conference 2012, which takes place between 28-30 March, is an opportunity for a full gathering of Chinese government officials and industry experts to discuss the state of the country’s cement sector. ICR will be in attendance and is keen to hear what might be expected in the next phase of China’s development.

Although construction continues to grow, cement producers are expected to see competition for markets intensify

Some priorities have already been made clear. In terms of China's cement sector development, the fast-track capacity expansion is now being surpassed by the need for enhanced cement quality and efficiency. The government has initiated a restructuring plan, replacing outdated capacity with modern production facilities and encouraging top cement producers to carry out mergers and acquisitions (M&A) to consolidate the industry. New capacity is now restricted to around 250Mta.

More recently, China’s environment ministry is set to take the lead for emerging countries in curbing industry emissions by implementing stricter rules on cement plant NOx emissions. In February, Reuters reported that the move could wipe out a third of the industry’s total net profits as it would be expensive to introduce. China’s strategy had been to cut overall NOx emissions by 10 per cent by 2015. Local press now expect the ministry to reduce NOx emission allowances from 800 to 400g/m3.

In addition, seven provinces are to set carbon emission caps as a prelude to establishing carbon trading markets in China. The government is currently required to reduce CO2 emitted per unit of GDP by 17 per cent by 2015. This is the first time that the Chinese government has called for any absolute caps on emissions, having preferred softer “carbon intensity” targets.

Economic slowdown starts

The speed of China’s economic growth in recent years has been remarkable. However, recent times have seen a slowdown. The rise in China’s industrial enterprise profits as a percentage of GDP peaked in 2007. In addition, only certain sectors have been able to maintain a growth environment since 2009: banking, transport, metals and mining have remained vibrant. Although GDP is expected to continue its strong growth path as private sector demand for high-quality goods consolidates, a deceleration to single-digit figures is now becoming more marked. In addition, the IMF forecasts GDP expansion at nine per cent for 2012 and 9.5 per cent annually during 2013-16, but the Chinese government has lowered its sights to seven per cent annually over the next five years.

According to Deloitte, monetary policy has seen China pump the equivalent of 50 per cent of GDP in the economy over 2008-10 through quantitative easing, which has kept the economy moving at a fast pace. This has now been bolstered by the 12th Five-Year Plan which came into effect in January 2011. It sets out a progressive way to achieve “inclusive growth” with more benefits filtering down to the greater proportion of Chinese citizens and gives more emphasis on agricultural sector growth. This means a shift in economic attention and development of the western provinces, and a greater focus on rural reform.

However, as the plan is all encompassing, it will also effect developments across the board – in energy, housing, transport, infrastructure as well as industries such as cement.

Energy and fuel

China is now the world’s largest energy consumer, which is putting further pressure on oil prices, although its oil consumption is only half that of the USA’s. Coal is the main energy source, but the government is keen to reduce its dependence on this fossil fuel and domestic coal output could be lowered to 3.6-4bnt by 2015.

The Bank of China International (BOCI) reports that coal prices bewteen 2000-10 have increased by 260 per cent. Coal is a major cost factor for most of China’s domestic cement producers. In 1Q11, China National Building Material (CNBM) subsidiaries China United, Southern Cement and North Cement paid on average CNY695/t, CNY780/t and CNY573/t, respectively. Meanwhile, the Sunnsy Group in the north records a 1H11 coal price of CNY731.90/t.

For 2012, the government has set a regulatory price cap of CNY800/t (US$127/t) for thermal coal used in cement production. The price ceiling will probably help cement manufacturers prolong the predominant use of coal, although producers are well aware that energy is their biggest production cost and an area where they can make savings. For producers like West China Cement relative coal costs have increased from 31.2 per cent of total production costs in 2009 to 37.4 per cent in 1H11.

By 2020, China expects 15 per cent of primary energy to come from non-hydro renewable sources such as wind and solar power. The 2015 target for non-fossil fuel energy use is 11.4 per cent. Hydroelectricity accounts for most of China’s renewable energy source, but by 2012 it is estimated that three-quarters of the country’s hydroelectric capacity will have been achieved.

Investment in nuclear power is targeted at five per cent of electricity needs by 2020 with 11 power stations in operation now and seven under construction.

State plan drives construction

Commodity housing, sold to private parties, has been predicted to dip in 2012. Property prices are already falling so less local government land is now being sold to property developers, meaning a slowdown in new buildings. This will reduce new housing construction, which has accounted for more than seven per cent of GDP in the last few years, according to Deloitte research.

However, the construction of 36m units of affordable houses on a budget of CNY1.3trn was among the central aims of the new five-year plan. Social housing is expected to increase cement demand by 3-7 per cent during 2011-13, if the government maintains its 10m unit construction rate target for 2011-12, says BOCI.

The social housing shortages are most acute in the north and southwest. The top five provinces in terms of demand are: Heilongjiang (N), Chongqing (SW), Shaanxi (NW), Inner Mongolia (N) and Hunan (Central). BOCI suggests that Anhui Conch – with its major capacity in Heilongjiang, Hunan and Chongqing provinces – will be one of the main beneficiaries. Sanshui Cement should pick up orders from Inner Mongolia, while social housing will help CNBM may bolster its sales in Hunan province.

Rapid urbanisation continues at a strong pace, especially in the south and southwest

Rapid urbanisation continues at a strong pace with high cement demand for housing, although in the long run the government’s high targeting is unsustainable. China has set an urbanisation rate of 51.5 per cent from 47.5 per cent, an increase of four percentage points on the 11th Five-Year plan.

The IMF forecasts that there will be 380m more inhabitants in China’s urban areas by 2030, taking the urbanisation rate to 70 per cent. This means China needs to build around 5m homes every year, but the government has targeted 10m affordable housing units for 2011-12. So construction is running well ahead of demand. Indeed, Société Générale reports: “With around 1.8bnm2 of new residential floor [already] completed in 2010, China has built the equivalent of Spain’s housing floor space stock.”

As the movement of people from rural areas to the towns continues, the government is doubling its investment in water conservation projects to CNY4trn over the next decade.

Favoured regions for construction growth are the east and south as there is less of a fall in new infrastructure projects in these areas. The main developments are expected in the provinces of Gansu, Jilin, Anhui, Fujian, Shanxi and Shandong. In terms of new fixed asset investment (FAI) project startups, it is eastern China that has seen the most robust growth of 44 per cent. This is good news for Anhui Conch and CNBM. Sinoma is set for a harder time in the north as more than a 40 per cent decline in project FAI startups is forecast by the BOCI for the provinces of Ningxia, Beijing, Inner Mongolia, Sichuan, Guizhou, Liaoning and Henan.

West China Cement has begun to supply the Southern Shaanxi Resettlement project that requires approximately 1.2-1.4Mta of cement between 2011-20 and the Hanjiangto Weihe River Water Transport project which also started construction in 3Q11 and will be completed in 2020. These large-scale projects will also be of value to other producers in Shaanxi such as Jidong Cement, Conch, Shengwei Cement and Italcementi.

Less-favoured regions for FAI project starts include, Ningxia, Beijing, Inner Mongolia, Sichuan, Guizhou, Liaoning and Hennan. This is where Sinoma is most exposed, although Shanshui Cement and Conch also have capacity there.

Infrastructure budget reduced

Macquarie Research has indicated that the 2008 peak surge in infrastructure financing is unlikely to be matched and it expects a spending decline from 2011. Indeed, there is great concern over the budget for high-speed rail projects, which may be reduced with a knock-on to cement demand in 2012. This would impact most on producers like West China Cement and Sinoma in the west.

However, highway building is a major requirement to developing the western regions. Despite its huge network of 74,000km of freeways, congestion and slow road haulage have hampered China’s domestic logistics and transport industry.

Among the development plans are the construction of seven new freeways originating from Beijing, nine new expressways running north to south and 19 “thruways” connecting east to west. Considering that 1200 townships and 120,000 villages had no paved roads at the end of 2010, it is staggering to believe that by 2015 the government’s objective is to make 90 per cent of all townships and villages accessible to vehicles.

In addition, by the end of 2012 the government aims to have increased the transport network, including rail, highways and ports, by 40 per cent.

Unsustainable cement consumption levels

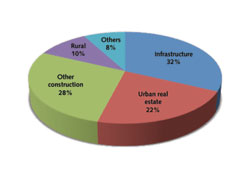

Figure 1: cement consumption by end-user

Cement consumption is forecast to improve during 2011-12 with the best areas being the southwestern, central-southern and central-northern regions. A breakdown of end markets for cement is given in Figure 1. The China Cement Association (CCA) expects cement demand to grow 12 per cent YoY to 2.1bnt this year. Taiwan Cement’s prediction for Chinese cement consumption is more conservative at approximately 7-8 per cent. Credit Suisse reports that there is less demand in the northeast and east.

China’s per capita consumption is now at 1400kg, but its sustainability is under question. Analysts are mindful of Spain’s 2007 per capita consumption of 1300kg which could not be sustained as the construction bubble burst. “Our analysis indicates that such high cement consumption is unsustainable and all countries where cement consumption has exceeded 1000kg per capita for a number of years has gone through a construction crisis sooner or later,” said Société Générale.

So cement consumption is likely to drop severely at some point in the near future. Société Générale predicts that it will be greater than the fall-off in construction activity, so a 20 per cent decline in construction might lead to a 40 per cent decrease in China’s cement consumption and, therefore, a 15-20 per cent reduction in global cement demand.

Cement producers compete for markets

By 2010 there were 18 enterprises in China with more than 10Mta cement capacity. The CCA states that some 253 production lines started construction in 2011 and are scheduled to come online in 2011-12, adding 318.4Mta of clinker capacity. By end-2012, China’s total clinker capacity will be 1.574bnta and cement capacity will reach 2.581bnta, according to CCA estimates.

Credit Suisse expects cement production to grow at 3-4 per cent to meet national economic needs during the period of the 12th Five-Year Plan. This means that maximum market needs will reach 2.4-2.5bnt in the next 5-10 years, according to the CCA. In 2011, China produced 1.87bnt of cement reports the CCA, while clinker production rose to 1.15bnt. Seven provinces recorded cement output above 100Mta.

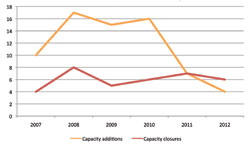

Figure 2: changes in cement capacity

(as share of consumption)

Meanwhile, further rationalisation of the sector is going ahead. China’s Ministry of Information and Technology (MIT) announced several aims for 2011-15, including the further retirement of outdated capacity. The schedule is to eliminate 250Mt of outdated capacity compared with 340Mt during the 11th year five-year plan. BOCI reports that elimination will continue most rapidly in Shandong, Guangdong, Hunan and Shanxi, while Guangdong’s government forecasts all its outdated capacity will be removed by the end of 2012. The Shanxi government predicted that it would eliminate 13.2Mt of old capacity in 2011. “The slowdown in new expansion, combined with the ongoing government effort in closing down old capacity, is paving the way for a cyclical upturn in 2011-12E,” reports Credit Suisse.

Industry consolidation among the top 10 players is also hoped to improve so that they account for 35 per cent of the market share by 2015 as oppose to 25 per cent today (see Table 1).

|

Table 1: clinker capacity of top 10 companies, end-2010 |

||

|

Company |

Clinker capacity ('000tpa) |

Market share (%) |

|

CNBM |

138,660 |

11.04 |

|

Conch |

110,490 |

8.80 |

|

Jidong Development |

49,570 |

4.08 |

|

Sinoma |

48,380 |

3.85 |

|

China Resources |

36,020 |

2.87 |

|

Huaxin Cement |

35,400 |

2.82 |

|

Taiwan Cement |

29,360 |

2.34 |

|

China Tianrui Group |

27,130 |

2.16 |

|

Sunnsy Group |

26,320 |

2.10 |

|

Jinyu Cement |

26,250 |

2.10 |

|

Total |

527,580 |

42.16 |

|

Source: China Cement Association |

||

Until the end of 2009, the proportion of state-owned business capital fell to 22.8 per cent, while foreign ownership was 25.6 per cent. Several multinationals have entered the Chinese market including, Lafarge, Holcim, HeidelbergCement, Italcementi, CRH, Cimpor and Taiheiyo.

Top producers on expansion drive

CNBM is China’s largest producer with a cement capacity of more than 250Mta. Its subsidiary South Cement has grown quickly by consolidating over 145 cement companies in southeast China in just three years and CNBM is looking to expand further. This will be achieved mainly via its subsidiary North Cement, which could increase its capacity by some 30Mta through mergers and acquisitions between 2010-13. CCB International Securities’ (CCB) analysts also forecast further expansion in southwest China. For now, CNBM has a dominant position in Jiangsu with its United Cement subsidiary and in Zhejiang province via South Cement, having effectively consolidated its position in eastern China where the group has 63 per cent of its capacity.

The 1.34Mta cement works at Ankang Xunyang helped

West China Cement’s total capacity rise to 16.2Mt at the

end of 2011. The company’s 1.1Mta Hanzhong Xixiang facility,

Shaanxi province, also commenced operations in April 2011.

In February 2012, West China Cement was scheduled

to commission a 1.5Mta second line at Shangluo

Danfeng, Shaanxi province

A big beneficiary from the acquisitions strategy has been BBMG, located in the northeast, which had a cement capacity of 40Mta at the end of 2010 and is targeting a capacity of 50Mta by the end of 2012 through further acquisitions. It is currently undergoing a merger proposal with Taihang Cement, increasing the group’s capacity by 5-7Mta.

State-owned Anhui Conch is the second-largest producer with a cement capacity of 150Mta in 2010 or 7.7 per cent of total Chinese capacity. Deutsche Bank estimates that Anhui’s annual clinker capacity growth will slow from 27 per cent in 2010 to 20 per cent two years later. The company expanded by 31Mta in 2011, with 19Mta coming from greenfield projects and 12Mta through M&A. Only some 15Mta of its domestic newbuild capacity is yet to come on-stream. Five new Anhui lines where scheduled to go online in 4Q11 and 1Q12, one 5000tpd line in Guangyuan, Guangxi and Qiyan, Hunan and three 2000tpd lines in Anhui province. The company’s most recent acquisitions have been in the provinces of Shaanxi and Guangxi, totalling 11Mta, according to Deutsche Bank.

Sinoma, through China National Material, prioritised M&A activity in 2011, investing some CNY21bn in capacity expansion. Sinoma’s sales volume was expected to increase by 30 per cent to 60Mt with a production capacity target of 100Mta in 2011, up 43 per cent YoY, according to HSBC research. Most of this growth is anticipated in the northwest.

As of 30 June 2011, the Sunnsy Group-owned Shanshui Cement Group Ltd had a total clinker and cement capacity of 32.39Mta and 69.94Mta, respectively. During 2011, the company opened a 4500tpd clinker line and 1Mta grinding capacity at Weishan Sanshui Cement and a 0.8Mta grinding plant for Balin Youqi Sanshui Cement, while acquiring the 0.6Mta plant of Inner Mongolia Lande Cement. The Sunnsy Group also opened several new companies and joint ventures in Shanxi, Shandong, Henan and Liaoning to develop its cement business.

Taiwan Cement expects its Chinese capacity to reach 60Mta in 2012 by targeting M&A activity and aiming to become a top 10 producer in China by 2016, although the CCA already believes it has reached the top 10 (see Table 1).

China Tianrui Group ranks 10th in terms of its clinker and cement capacity, which stands at 22.2Mta and 35.2Mta, respectively. It is the top producer in Henan and Liaoning provinces and has gained government support for further M&A consolidation, which can be expected in the central and western regions.

Main areas for capacity growth

CCB analysts predict the cement capacity additions in the east will rise by an additional 72Mta in 2012F or 12 per cent YoY. Lighter capacity additions are forecast for Zhejiang (1.5Mta) and Jianggxi (6.2Mta) in this period. In the southwest, Lafarge is the largest cement producer with 19Mta clinker capacity, followed by United Cement with 10Mta.

However, CCB reports that CNBM has acquired around 100 local producers in the southwest to form a new subsidiary, South West Cement, bringing 100Mta of capacity consolidation to the newly-formed company over the next few years. CNBM also acquired Lisen Cement and Kehua Group with a total cement capacity of 18Mta in Sichuan and Chongqing at the end of 2011.

Looking at the near term, Credit Suisse estimates that new cement supply (capex projects) will fall from nearly 300Mt or 16 per cent in 2010, to 136Mt or seven per cent in 2011 and potentially 90Mt or five per cent in 2012 (see Table 2).

|

Table 2: Chinese cement supply/demand model |

|||||||||

|

New cement capacity |

2007A |

2008A |

2009A |

2010E |

2011E |

2012E |

2013E |

2014E |

2015E |

|

New dry kilns (Mta) |

796 |

1036 |

1298 |

1594 |

1730 |

1821 |

1901 |

1981 |

2061 |

|

Vertical kilns and others (Mta) |

742 |

627 |

548 |

448 |

310 |

175 |

175 |

175 |

175 |

|

Total capacity (Mta) |

1538 |

1663 |

1846 |

2042 |

2040 |

1996 |

2076 |

2156 |

2236 |

|

YoY change (%) |

5 |

8 |

11 |

0 |

-2 |

4 |

4 |

4 |

4 |

|

Net capacity change |

|||||||||

|

New dry kilns (Mta) |

128 |

239 |

262 |

296 |

136 |

91 |

80 |

80 |

80 |

|

Vertical kilns and others (Mta) |

-53 |

-115 |

-79 |

-101 |

-138 |

-136 |

0 |

0 |

0 |

|

Net capacity change (Mta) |

75 |

124 |

184 |

195 |

-1 |

-44 |

80 |

80 |

80 |

|

Average utilisation (%) |

90 |

86 |

93 |

94 |

94 |

98 |

102 |

101 |

101 |

|

Production |

|||||||||

|

New dry kilns (Mta) |

745 |

862 |

1108 |

1373 |

1579 |

1740 |

1954 |

2038 |

2122 |

|

Vertical kilns and others (Mta) |

609 |

520 |

524 |

463 |

333 |

231 |

124 |

105 |

93 |

|

Total production (Mt) |

1354 |

1382 |

1632 |

1837 |

1912 |

1971 |

2079 |

2143 |

2215 |

|

YoY change (%) |

12 |

2 |

18 |

13 |

4 |

3 |

5 |

3 |

3 |

|

Trade and demand |

|||||||||

|

Exports (Mt) |

33 |

26 |

16 |

16 |

16 |

16 |

16 |

16 |

16 |

|

Apparent demand (Mt) |

1321 |

1356 |

1616 |

1820 |

1896 |

1954 |

2062 |

2127 |

2199 |

|

YoY change (%) |

13 |

3 |

19 |

13 |

4 |

3 |

6 |

3 |

3 |

|

Source: Credit Suisse estimates, China Cement Association, company data |

|||||||||

Currently, MIT has suspended the approval process for new projects with the exception of eight 2500tpd lines to be built for Xingjiang. There is still 150-200Mt of new capacity that has already received approval and is presently under construction. Credit Suisse estimate that 70 per cent of this capacity will have come online in 2011 and the remainder will follow in 2012. Of course, MIT could also resume the approval process at any time.

Cement prices

In terms of cement prices, the eastern region outperformed in 2011, while the overall domestic price saw an upswing in 1Q11, up 19 per cent YoY. Eastern China had price hikes of 60 per cent or CNY513/t (US$81.30/t) compared to the national average of 18 per cent or CNY431/t (US$68.30/t). Most other regions also saw cement prices rise in 2011 with the exception of the southwest where they fell below CNY400/t.

Prices are lowest in the southwest because of overcapacity and intense competition among producers. The region’s market is highly fragmented with the top 10 producers accounting for 34.9 per cent of sales. Total cement production in the southwest reached 260Mt, up 30.9 per cent YoY in October 2011, making it the fastest-growing regional market, according to CCB.

However, as the larger regional cement conglomerates acquire a greater share of cement production through M&As it can be assumed that their control over cement prices will become greater. This can already be seen in eastern China, which has seen the most rapid large-scale consolidation among producers in the last three years, led by CNBM and Anhui Conch. The top 10 producers’ market share here was at 60 per cent by the end of 2010 and average prices have surged 41.2 per cent YoY, while margins have also improved for the top producers in the east.

While BOCI acknowledges that cement prices have been relatively cheap in recent times, the bank predicts that going forward, they will receive strong support as a potential for easing of oversupply exists. In Sichuan and Chongqing, prices are expected to rise 5-10 per cent in 2012.

Exports

Anhui Conch reduced itsclinker and

cement exports in 2011 as domestic

demand remained high

In August 2011, the MIT stated that cement and clinker exports were down in 1H11 by 35.5 per cent to 5.6Mt as a result of high domestic cement demand. Between January and October, China Customs Statistics reported that combined exports rose to 9Mt, down from 14.4Mt a year earlier, although prices for exports have risen YoY. Export sales were only three per cent of Anhui Conch’s sales volume in FY11E.

Conclusion

It had seemed that China was immune to the turmoil occurring in the rest of the world’s economies, but it too is starting to feel the effects of a slowdown from the extreme growth patterns it has generated in the last few years. It is paramount that the cement industry is ready for the adjustment, because when construction orders do fall off, cement orders will be next to suffer.

Government funding for infrastructure projects, social housing and water conservation are assured, but they are leading growth at a faster rate than is really required. In essence, by implementing its five-year plans to stimulate growth the government’s strategy distorts the level of true demand and sets its own agenda. However, when housing demand is supplied more than twice-over, the industry has to react by decelerating construction for demand to catch up.

The prestigious China International

Cement Industry Exhibition

A major question that the industry must face is how sustainable is the continued increase in domestic cement capacity? Even the MIT can see it is not sustainable and has put a cap on the amount of new capacity projects to bring them under greater control. Stricter regulations over emissions are also set to come in as the cement industry is reformed and outdated capacity is removed.

One also wonders how easy it will be for the top 10 producers to forward their plans for consolidation with a forecast slump in domestic construction in the not too distant future. Depending on how easy finance is to obtain through bank loans and share offerings, the path that Anhui Conch has taken to expand its cement production base overseas might well be an example that other leading Chinese producers could yet follow in greater numbers.

It will be intriguing to see what delegates attending the 13th China International cement Industry Exhibition and Conference in March will feel about the latest trends in the Chinese cement sector and if there are many solutions offered. We hope to see you there.

Article first published in International Cement Review, March 2012.