Brazil: future secured?

The expansion of Brazil’s cement production base continues unabated despite storm clouds gathering on the economic horizon. However, this Latin American giant still requires the construction of infrastructure and housing to support its national development and the future of the cement industry appears guaranteed.

Cimento Portland Partipações (CPP) has plans for four new cement plants. Pictured is the São Luis works, completed

in November 2014 by FLSmidth. CPP is now preparing the environmental stage of its Paripiranga unit in Bahia

Brazil’s cement sector is still speeding ahead in terms of plant capacity expansion. Brazilian cement association Sindicato Nacional da Indústria de Cimento (SNIC) estimates that demand could hit 100Mta by 2020 in the country with an average YoY economic growth rate of six per cent. However, the latest data available suggest a more modest performance. The IMF forecasts that GDP growth will expand from 1.4 per cent in 2015 to 3.1 per cent by 2019, while independent consultant Monica de Bolle suggests greater caution is in order, with GDP growth at turning negative, and both the construction and cement industry impacted.

However, there are some positive signs in the construction industry. Among the drivers underpinning demand are massive projects like the Olympic Games, to be held in Rio in 2016, and infrastructure projects for the construction of dams and highways as well as rail transportation and the expansion of ports and harbours.

Rising demand

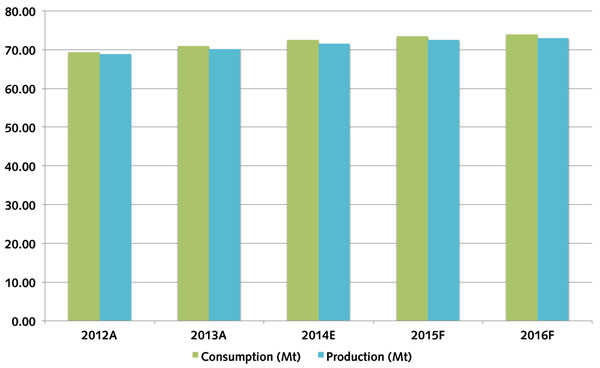

Over the past three years, cement consumption in Brazil has been rising and is expected to reach 74Mt in 2015, up from 69.3Mta in 2012, according to the forthcoming Global Cement Report Eleventh Edition (see Figure 1).

Figure 1: Brazilian cement consumption and production, 2012A-16F

The main end markets are housing, which accounts for 58 per cent of consumption, followed by infrastructure (25 per cent) and non-residential building (17 per cent).

Bagged cement accounts for

nearly two-thirds of the market

The Brazilian market is developing fast and while transport is difficult across vast regions, some 96 per cent of cement is moved by road, three per cent by rail and one per cent by ship.

Bulk cement only accounts for 34 per cent of deliveries with bagged cement by far the predominant form of buying cement, accounting for 66 per cent of sales.

Fast-developing production base

There are now 56 cement plants and 32 grinding facilities in Brazil with a domestic cement capacity approaching 88Mta. The giants of the local industry are Votorantim Cimentos, which has the largest market share (36 per cent in 2014) with 32.5Mta of domestic cement capacity at the end of 2014, and Camargo Corrêa’s InterCement Brazil, which also ranks highly with 16 production units and a 20 per cent share of the market.

Brazilian-owned cement companies have significantly grown in size in the past few years and have become increasingly powerful. InterCement, a fully owned subsidiary of Camargo Correa (Brazil), completed its acquisition of Cimpor in 2012, and now operates 17.9Mta of capacity in Brazil, combining the operations of Camargo Correa and Cimpor in one business unit: InterCement Brazil. Moreover, the company invested E128m in its Brazilian cement operations in 2014 by increasing capacity of the cable car system at the Apiaí plant (São Paulo), adding a waste fuel burner system to the Candiota works and by investing in new cement capacity at the Caxitu unit, as well as modernising the brownfield Cezarina cement facility with a new production line.

The only foreign-owned cement majors now operating in Brazil are Lafarge and Holcim with nine and five cement facilities, respectively. However, with the forthcoming merger between the two groups this situation is likely to change with CRH in line to acquire assets being disposed of in Brazil, among other countries. The Brazilian operations to be purchased include three integrated plants, two grinding stations and some ready-mix operations.

Expansion plans

News of further cement capacity expansion has been slower than in recent years, but there are some new projects underway. One of these is at Cimento Apodi, which only started producing cement in 2011 from its 0.36Mta grinding plant in Pecém at the port of Apodi. Based 63km from Fortaleza, in the north of the country, the company uses clinker imports from China as well as locally-sourced slag. To unload raw materials at Apodi, the company uses a B&W Mechanical Handling (Aumund Group) Eco Hopper. The grinding unit operates with a FLSmidth OK 25-3 vertical roller mill for the production of ground slag.

Cia. de Cimento Itambé’s OK™ 33-4 mill is up and running at

the Balsa Nova plant. The mill successfully commissioned by

FLSmidth in 2014, and is meeting guarantees

This unit was followed by a second works in 2013 when Cimento Apodi opened an 1800tpd integrated facility in Quixeré, Ceará state, some 214km from Fortaleza. The company mooted further expansion plans in August 2014 when it announced a new 3.3Mta integrated plant in Santo Amaro, Brotas, in the northeastern coastal state of Sergipe. The greenfield plant will cost BRL1bn.

However, market leader Votorantim remains by far the biggest investor in Brazilian cement capacity with 25 per cent of its BRL2.5bn capex budget allocated to capacity expansion, focussing on the northeast, north and midwestern markets. In 2014 Votorantim Cimentos moved ahead with the biggest investment plan in its history, launched in 2007, and will reach BRL11bn by 2016, in addition to the 8/18 plan, which consists of adding 8Mta of production capacity by 2018.

During 2014 Votorantim inaugurated the 1.2Mta Cuiabá plant and completed the 1Mta Rio Branco expansion as well as the BRL72.2m Santa Helena (São Paulo) upgrade, which saw a new 0.7Mta cement mill installed. Current expansion projects include a 1.2Mta plant in Primavera, a 1.9Mta works at Edealina and a 0.8Mta production facility at Xambioá. Its most recent project launch was at Caaporã, Paraíba, where it is building a 2Mta greenfield plant, scheduled for commissioning in 2017. This project costs BRL700m.

“The logistical structure of the state, which includes the Port of Cabelelo, the significant market growth of the northeast region, and a government partnership for the concession of tax incentives, were some of the determining factors in the choice of Paraíba for the new manufacturing unit of Votorantim Cimentos,” said Edvaldo Rabelo, global executive director of energy, sustainability and safety at Votorantim Cimentos.

The Caaporã unit will be Votorantim Cimentos’ sixth cement factory in the northeast region. The other units are located in Ceará, Maranhão, Pernambuco and Sergipe. In Ceará Votorantim is building two new lines at Sobral and Pecém, to be called Sobral II and Pecém II, respectively. The Sobral expansion will begin construction in May 2015 with the Pecém project to follow in July 2015. The projects will double the combined capacity of the two works to 6Mta.

Votorantim-owned Mizu Cimento put its second mill into operation at the Baraúna plant, Rio Grande do Norte, in September 2014, doubling the works’ capacity to 2.4Mta. Earlier in May the 3000tpd second clinker line was started up by Hefei Cement Research & Design Institute (HCRDI). The second line project was jointly undertaken by HCRDI and Inner Mongolian Northern Heavy Industries group (NHI). It was the first EP project that HCRDI had secured in South America.

Lafarge Brasil has also been active on the capacity build front, having inaugurated its Santa Cruz plant in February 2014 to mainly serve the Rio de Janeiro region. The integrated facility was expected to produce 0.5Mt in 2014 and 0.75Mt in 2015.

Meanwhile, Fives FCB is supplying Holcim (Brasil) with a new 4500tpd line at the Barroso plant, Minas Gerais. Work started in April 2012 and as at 5 March 2015 was 83 per cent complete. The BRL1.7bn expansion will raise the facility’s cement capacity from 1.2Mta to 3.6Mta. Upon completion, Holcim aims to distribute cement into the major markets of São Paulo and Rio de Janeiro. Barroso is situated close to the cities of São João del Rei, Tiradentes and Barbacena. A particularly challenging part of the project has been the transport of raw materials from the Capoeira Grande and Ribeirão Mata mines to the plant. A 7.2km ‘Flyingbelt’, supplied by Agudio of Italy, has helped overcome this obstacle, enabling Holcim to transport some 1500tph of crushed limestone and clay to the cement works (see ICR January 2015).

In addition, crushing capacity will increase from 180tph to 450tph. The Fives FCB Horomill 440 raw mill does not use water and benefits from low power consumption, while the cement mill will have a capacity of 450tph and the multi-mill drive is to be supplied by Gebr Pfeiffer. The new preheater rises 130m and it will help enable clinker capacity to be raised from 2000tpd to 6500tpd. A modern and fully-automated quality control lab is also being installed. Two new cement silos are being constructed to hold 10,000t and 21,000t of cement, while the clinker silo will have a capacity of 35,000t. Furthermore a 72.5m-high raw material silo will have a 10,000t capacity.

Local competitor CSN has not found it easy to expand its cement production base, but it is to build a 3Mta integrated plant at Arcos, Minas Gerais. This will increase its market share from the current three per cent. The plant should be operational by the end of 2016, according to Luiz Fernando Martinez, CSN executive director.

From its existing 2.4Mta Volta Redonda plant, CSN mainly serves the Rio de Janeiro (South Fluminense) and Paraíba Valley (SP) markets. It faces competition primarily from Votorantim, InterCement, Holcim, Lafarge and Cimento Tupi. The new plant, which will produce Type CP-3 cement with less slag than the Volta Redonda product, will enable the company to expand further into Minas Gerais, São Paulo and Rio de Janeiro.

Also expanding is Cimento Tupi which currently operates 3.2Mta of cement capacity at its Pedra do Sino plant, Minas Gerais. The company is constructing a 1.5Mta greenfield plant in Paraná which will be commissioned in 2016.

Furthermore, Grupo João Santos-owned Cimento Nassau has invested BRL68m in the modernisation of its Itaguassu works in Sergipe.

Meanwhile, Cia de Cimento Itambé’s has contracted ThyssenKrupp Industrial Solutions to supply a new 3300tpd line at its Balsa Nova plant together with a 265tph Quadropol raw mill. FLSmidth supplied an OK-33 mill for cement grinding, scheduled for commissioning in 2015.

New players set up shop

In addition to upgrades and new plants by existing producers, Brazil’s cement sector has attracted several new entrants. One new player is Companhia Vale do Ribeira (CVR), which drew up a contract in December 2013 with Chinese CITIC-HIC for a 1Mta cement plant at Adrianople, Paraná, involving an investment of BRL518m. Construction work on the facility is scheduled to start this year and should take around 30 months to complete.

“We decided to invest in the city for its strategic location on the border with São Paulo, which is the largest consumer market in the country, by the availability of raw material and the ease of production,” explains Henrique Bica Zaffari, senior associate director of CVR.

Arabian Cement has entered a joint- venture agreement with Cementos Relampago (Cementos La Unión Group) for a 0.23Mta plant in the northwest. The Egypt-based producer will fund EUR7m of the total plant cost of EUR23m.

The union of two Brazilian groups – Queiroz Galavão and Cornelius Brennand – formed the Portland Cement Holdings group or Cimento Portland Partipações (CPP), which markets its product under the Cemento Bravo brand. This group has plans for four plants – three integrated and one grinding works – to be located in the northeast, midwest and southeast Brazil.

Following the establishment of the São Luis plant in November 2014, the CPP group is working on the environmental phase of its second unit in Paripiranga, Bahia, about 370km from Salvador. The BRL850m Cementos da Bahia plant will be an integrated works with a cement capacity of 2Mta and will serve the markets of Bahia, Sergipe, Alagoas, Pernambuco and Paraíba, extending to Rio Grande do Norte and Ceará. The remaining two works will be located in the southeast and central-east of the country.

Brennand Cement is nearing completion of its greenfield 3300tpd Pitimbu plant, Paraíba state, which FLSmidth is constructing.

Cimento do Maranhão (CIMAR) opted for a new 0.5Mta slag grinding unit at São Luis, installed by Fives FCB

The new 0.5Mta slag grinding plant in São Luis for Cimento do Maranhão SA (CIMAR) is equipped by Fives FCB with an FCB B-mill of 3400kW, a third-generation FCB TSV™ classifier 3200HF and a Sonair™ process filter. The equipment is capable of operating at 80tph to produce cement with 30 per cent slag at 3800Blaine. This grinding unit is strategically positioned 13km from the port of Itaqui, and has a rail connection for raw materials and cement distribution, but it can also bag cement at a rate of 3600 bags/h. The main markets for the CPII-E-32 type produced cement are São Luis, Maranhão, Piauí and Pará. The plant uses slag from the steel works in Açailândia in its cement production, while clinker is imported via the port of Itaqui where the company operates two eco hoppers. Four cement storage silos at the plant have a capacity of 1500t each.

Cartel fines

It has not all been profits though, especially for cement producers that were hit by competition watchdog Cade’s US$1.4bn fine for price fixing over two decades. Votorantim, Camargo Corrêa SA’s InterCement, Itabira Agro Industrial SA, Cia de Cimentos Itambé, Holcim, Lafarge and Cimpor were accused of setting prices to force others out of the market and even the industry associations of ABCP and SNIC have had sanctions imposed on them by Cade. As appeals are likely by the companies concerned, further time in the courts is expected.

Modest trade

In recent years Brazil’s imports have been fairly minimal at around 1Mta of cement and 1.5-2Mta of clinker. Some clinker has arrived from under-utilised Iberian plants such as Cementos Cosmos’ Toral de los Vados factory, which sent 35,000t of clinker to Brazil in 2014. Spain accounts for 47 per cent of clinker imports, followed by Portugal (22 per cent), China (19 per cent) and Turkey (12 per cent).

Exports are similarly low in quantities but register about 20,000t of cement and 100,000t of clinker. Some 45 per cent of exports are destined for Bolivia, and a further 45 per cent to Paraguay while the remainder is delivered to Colombia. The main exporters are Grupo Nassau, which delivers to Colombia, Votorantim (Bolivia) and InterCement (Paraguay).

Outlook

The Brazilian cement market has grown at a CAGR of 7.7 per cent between 2003-13, according to Cimpor. While such growth has slowed in the past 12-15 months with GDP stumbling to little more than one per cent, the country still has the fifth-largest cement market in the world, with investment in new capacity ongoing as the northeast and the cities of São Paulo and Rio de Janeiro set the pace of cement demand.

The way ahead is not without its challenges. The worsening economy and the Petrobras scandal have meant strong headwinds for the country’s government. The slowdown in the construction industry has led to lay-offs, which have added to the administration’s popularity woes. However, the cement industry remains resilient and is expected to fight the Cade verdict. In addition, Brazil is in need of further airports, hospitals and improved housing for the disadvantaged. These key requirements for national development are forecast to send domestic cement demand upward rather than plummet to the depths that the temporary economic and political storm suggest.

Article first published in International Cement Review, May 2015.