European Union economics and the disconnect between the Northern and Southern construction markets: Dasha Lukiniha, IHS (UK)

Filmed at Cemtech Europe 2015, 20-23 September, Intercontinental Hotel, Vienna, Austria.

Login Required

A full subscription to International Cement Review Magazine is required to view videos. If a clip is available it will play below, otherwise please login to watch the full video.

Thank you very much for the introduction and for an opportunity to speak here, as Keith mentioned my name is Dasha and I work for IHS, a global forecasting and analytics provider. So today I'd like to talk to you about European Union economics and the disconnect that we're seeing between the Northern and the Southern construction markets and really where the next spots spot and the weak spot are going to lie, for the construction industry, for the building materials providers and for the cement suppliers in particular.

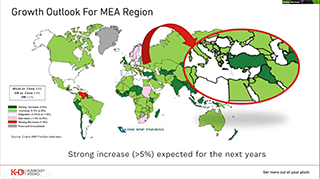

So first I'm going to go over the link between the construction and macroeconomic recovery, and how these two follow together, and how this unfolds within the European Union in general. And then I'm going to ask a question of is the trend really uniform across the region, or are there any hotspots within the lumber market, the cement market, the construction industry, and any weak performance, where we don't expect to see much growth, within next, over the medium term really. And then I'm going to hold in on the Northern European market, as one of the stronger performance and the Southern European market as one of the ones still battling the recession.

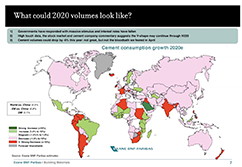

I'm going to slightly touch upon the Eastern European market as I think in the recent events, it's becoming one of the interesting construction and macroeconomic regions to look at and to see where the risks lie within the region. And then I'm going to tie this in together and say what this means for the construction industry going forward and what this means for the cement industry in particular. So I'm going to start off with this graph that shows construction spending against GDP growth and I'm going to almost state an axiom and say that construction spending tends to follow macro economic recovery very closely.

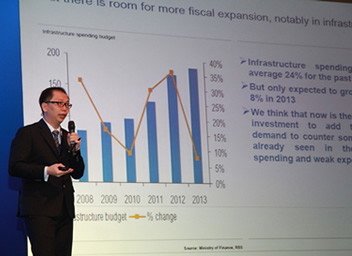

This happens due to a variety of reasons. First of all on the residential segment, construction spending really depends on consumer spending power, on the ease with which it is easy to get a mortgage, etc and on the non-residential side on the infrastructure and structures construction, it really depends on the health and the state of the budget, on how the government is able to plan for the large scale infrastructure projects over the near-medium term.

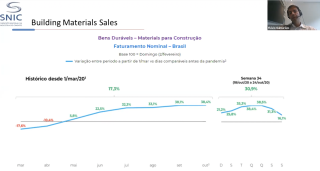

And looking at Europe it is by no means an exception, what we've seen is construction closely followed the GDP growth, GDP being slightly less cyclical, due to the fact that it includes an aggregate of all industries within the economies. So going forward we see this length continuing and for Europe as a whole we see stable growth rates coming out within the next two years.

So we see about a 1.5% growth this year and acceleration to 2% in 2016. Photo construction spending is going to follow suit and going to increase at a 2% growth rate, this and next year. If we were to look at the construction industry by different types of segments, so if we were to break it out and to the residential segments, so the housing demand and the non residential segment, your usual more cement intensive segment of the construction sector, it is generally quite a fairly balanced recovery.

Residential construction tends to recover quicker because housing demand tends to be more elastic, than government budgets for large scale infrastructure projects. Generally speaking we are seeing a pick up in both segments especially from next year on wards, which is going to drive the cement demands upwards in terms of the operating environment for the cement suppliers and producers, we see them operating in a stable custom environment, which is is a lot Jude festival all price drops, which is going to create a favorable effect for the margins for the suppliers, as well as a relatively low inflation environment.

So all in

all if we were to look at a European region as a whole, it looks like a stable and a fairly predictable market to invest in for building materials providers

That was just a 5 minute clip, to watch the full length video please login.

You need to have an active subscription to International Cement Review magazine to gain access, subscribe today for just just GBP£190.00, USD$315.00, EUR€250.00 for 12 months.

So first I'm going to go over the link between the construction and macroeconomic recovery, and how these two follow together, and how this unfolds within the European Union in general. And then I'm going to ask a question of is the trend really uniform across the region, or are there any hotspots within the lumber market, the cement market, the construction industry, and any weak performance, where we don't expect to see much growth, within next, over the medium term really. And then I'm going to hold in on the Northern European market, as one of the stronger performance and the Southern European market as one of the ones still battling the recession.

I'm going to slightly touch upon the Eastern European market as I think in the recent events, it's becoming one of the interesting construction and macroeconomic regions to look at and to see where the risks lie within the region. And then I'm going to tie this in together and say what this means for the construction industry going forward and what this means for the cement industry in particular. So I'm going to start off with this graph that shows construction spending against GDP growth and I'm going to almost state an axiom and say that construction spending tends to follow macro economic recovery very closely.

This happens due to a variety of reasons. First of all on the residential segment, construction spending really depends on consumer spending power, on the ease with which it is easy to get a mortgage, etc and on the non-residential side on the infrastructure and structures construction, it really depends on the health and the state of the budget, on how the government is able to plan for the large scale infrastructure projects over the near-medium term.

And looking at Europe it is by no means an exception, what we've seen is construction closely followed the GDP growth, GDP being slightly less cyclical, due to the fact that it includes an aggregate of all industries within the economies. So going forward we see this length continuing and for Europe as a whole we see stable growth rates coming out within the next two years.

So we see about a 1.5% growth this year and acceleration to 2% in 2016. Photo construction spending is going to follow suit and going to increase at a 2% growth rate, this and next year. If we were to look at the construction industry by different types of segments, so if we were to break it out and to the residential segments, so the housing demand and the non residential segment, your usual more cement intensive segment of the construction sector, it is generally quite a fairly balanced recovery.

Residential construction tends to recover quicker because housing demand tends to be more elastic, than government budgets for large scale infrastructure projects. Generally speaking we are seeing a pick up in both segments especially from next year on wards, which is going to drive the cement demands upwards in terms of the operating environment for the cement suppliers and producers, we see them operating in a stable custom environment, which is is a lot Jude festival all price drops, which is going to create a favorable effect for the margins for the suppliers, as well as a relatively low inflation environment.

So all in

all if we were to look at a European region as a whole, it looks like a stable and a fairly predictable market to invest in for building materials providers

That was just a 5 minute clip, to watch the full length video please login.

You need to have an active subscription to International Cement Review magazine to gain access, subscribe today for just just GBP£190.00, USD$315.00, EUR€250.00 for 12 months.