Freight rates firm up after initial dip

Selected freight market trends 20.06-04.07.2012

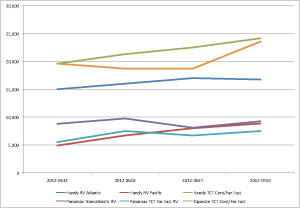

In the Panamax segment, prices rose in the week ended 20 June, but then fell back the subsequent week, reflecting a lower demand for coal and steel production in the western hemisphere. “Added by a question mark to Chinese imports for both coal and iron ore, the overall sentiment is not only affected by oversupply,” says shipping broker Fearnleys. Although Panamax rates generally recovered (to US$7500/day) for the TCT Far East RV by 4 July, in Transatlantic RV contracts fell short by around US$500 when compared with the start of the fortnightly period, registering at US$9250/day.

The Capesize market held little promise for shipping between 14-20 June as rates fell yet again but have since recovered at varying degrees. In the TCT Cont/Far East area, rates advanced from US$18,700/day on 20 June to US$23,550/day on 4 July. Tonnage rates also proved marginally more expensive as they rose from US$6.00/t to US$6.30/t on the Richards Bay/Rotterdam route during the same period. However, ships entering the market are too many for the cargoes available although iron ore and coal volumes remain good.

Meanwhile, the Baltic Dry Index appears to be recovering steadily as it climbed from 902 on 13 June to 1103 on 4 July.

Published under Cement News