Politics dominates the energy market, oil stabilises but coal drifts lower while petcoke rises on lower freight rates

By Frank O. Brannvoll, Brannvoll ApS, Denmark

The oil price remains subject to a risk premium due to the Israel-Gaza conflict. Providing the situation does not escalate, the market hovers around US$80. Meanwhile, the Ukraine-Russia war is still deadlocked, but the political stage in Europe and potential US election is lurking, making negotiations more likely.

In the financial markets both the European Central Bank and the US Federal Reserve have kept rates unchanged and have a two per cent inflation target for a longer period, taking away any imminent hopes of rate cuts. Furthermore, increased risks are seen from China’s property market with a large fund declared bankrupt. The markets are currently awaiting actions from the Chinese central bank and government, which could considerably impact energy demand. The Turkish central bank raised rates again by 2.5 per cent to 45 per cent to fight inflation.

The euro-US dollar fell to US$1.075 from US$1.09 but remains in the range of US$1.06-1.10. Brannvoll ApS maintains a range of US$1.00-1.15, with an average of US$1.10 in 2024.

|

Table 1: Prices at a glance - 7 February 2024 |

||

|

Crude oil (US$/bbl) |

79.00 |

|

|

Coal |

API2 – 2Q24 (US$) |

92.00 |

|

API2 – Cal 2025 (US$) |

97.00 |

|

|

API4 – 2Q24 (US$) |

93.00 |

|

|

API4 – Cal 2025 (US$) |

98.00 |

|

|

Petcoke |

USGC 4.5% 40 HGI – FOB (US$) |

73.00 |

|

USGC 4.5% 40 HGI – CFR ARA (US$) |

94.00 |

|

|

USGC 6.5% 40 HGI – FOB (US$) |

67.00 |

|

|

USGC 6.5% 40 HGI – CFR ARA (US$) |

88.00 |

|

Oil

OPEC+ will have a meeting in March to discuss the continuation of their production cuts. The risk of tensions spreading in the Middle East maintains the US$2-3 risk premium on the oil price. Downward pressure is coming from fear of weaker demand from China and from slowing economies as rate cuts are seen further ahead. When prices are firming, US production is increased, keeping a lid on any upticks for the moment.

The trading market has been kept in a narrow range and is expected to be US$77-85. Brannvoll ApS lowers forecasts to a trading range of US$70-100, with an average of US$90 for 2024.

Coal

The coal market drifted lower and again fell below US$100, pressured by lower gas and oil prices and an abundant coal supply.

Stocks are still high both in Europe and Asia, while European and Chinese domestic demand has fallen, sending prices further down. Meanwhile, Russia has removed its export fee, which depended on the US$/RUB exchange rate for coal, and this has further taken pressure off prices.

The API2 front-quarter (FQ) contract fell by 14 per cent MoM to US$92, lowering the short-term range of US$85-105 in its downtrend channel. The API2 Cal25 contract remained unchanged at US$97. Brannvoll ApS forecasts a range of US$100-130 and average of US$125 for Cal25, seeing the current level as major support.

The API4 FQ contract slid six per cent MoM to US$93, lowering the short-term range of US$85-100. The API4 Cal25 contract was unchanged at US$98. Brannvoll ApS expects a range of US$100-150 in 2024 as volatility is higher in API4.

Petcoke

Petcoke saw an uptick in January due to lower freight rates and several companies chasing Q1 material after New Year.

As production was lower a sharp price increase took place and the high sulphur product rose to US$72, before sliding back as demand declined.

Turkish cement producers were seen in the market, moving more towards Venezuelan petcoke. Venezuelan offers have pressured prices with offering material below market. However, increased offering may be expected in the coming months as Venezuela may want to sell more now in case US sanctions are reinstated on 18 April. The US demands free and fair elections in Venezuela in order not to impose sanctions again.

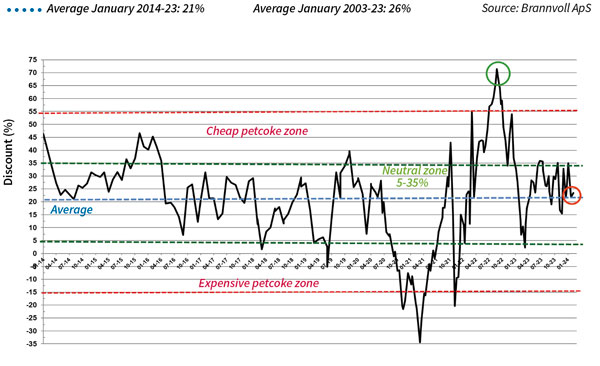

Petcoke discount to coal – API2 USGC 6.5% USGC ARA based on 6000kcal: Feb 2024: 23%

The USGC FOB 6.5 per cent sulphur (S) contract rose 12 per cent MoM to US$67, while the discount to API4 fell to 42 per cent. The USGC ARA 6.5 per cent S contract rose one per cent MoM to US$88 but the discount fell to 23 per cent, due to lower coal prices.

The USGC FOB 4.5 per cent S contract rose 12 per cent MoM at US$73, with the discount to API4 down to 37 per cent. The CFR ARA 4.5 per cent contract rose by two per cent MoM to US$94, staying below US$100 with the discount falling to 18 per cent.

At these levels petcoke is back in the neutral zone compared to coal but could be seen higher if coal is lifted back above US$100.

Published under Cement News