During 12-15 February 2012, over 250 senior cement industry delegates convened in Dubai, UAE, for the annual Cemtech Middle East & Africa (MEA) Conference and Exhibition. Now in its seventh year, the meeting was widely regarded as the best event to-date, offering participants a series of high-quality presentations, a host of networking opportunities including an international exhibition, as well as technical workshop and plant tour – all against the backdrop of exceptional hospitality.

A packed conference hall listens to presentations by speakers from all corners of Africa and the Middle East

Returning to the five-star luxury of the Grand Hyatt Hotel, Dubai, UAE, Cemtech MEA 2012 attracted some 250 delegates from 34 countries all keen to discuss the latest cement developments under the theme of ‘Growth markets, technology advances and operational efficiency’. This year’s Cemtech meeting provided a timely opportunity for those operating in the MEA region to listen to a host of expert speakers, take stock of recent economic and political events, particularly in the aftermath of the Arab Spring, and identify future development trends. A number of notable cement projects – including new capacities and operational improvements – were also brought to the forefront, highlighting the application of best technology in practice while further technical content explored advances in all aspects of cement manufacture.

MEA markets: trends & prospects

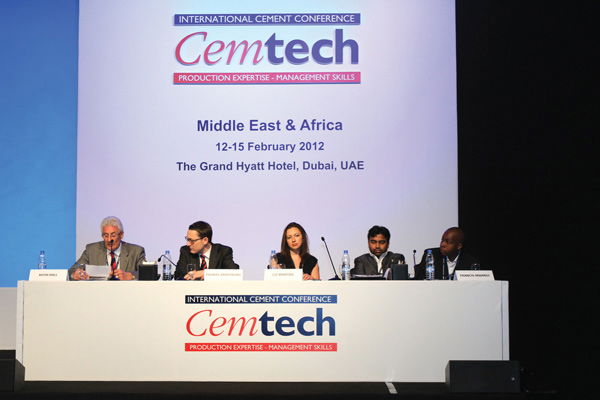

Left to right: Keith Hall, conference chair; Tom Armstrong, Cemtech organiser;

Liz Martins, HSBC; Hettish Karmani,Global Investment House and

Francis Mwangi, Standard Bank, Kenya

In light of a troubled global economic environment, Liz Martins of HSBC Bank, Middle East, took a close look at the risks facing the MENA region in 2012, with important implications for businesses. Here she discussed the impact the Arab Spring will have on policy making and what effect fear of conflict with Iran will have on sentiment and economic performance. From a global perspective, she explored how much likely damage a European recession will have on the real economy.

Honing in on the GCC cement sector, Hettish Karmani of Global Investment House (GIH), Kuwait underlined that while billions of dollars worth of development plans will keep demand progressing, a pick-up in demand in the UAE is essential for the region as a whole. GCC per capita consumption is the highest in the world but the region’s projects market has declined continuously from a heady US$2.5trn in 2008 to US$1.8trn currently. As at end-2011, total projects on hold were worth US$475bn (25 per cent of total projects). Saudi Arabia is the country with the most active projects at US$584bn. Cement capacity, meanwhile, reached 116Mt in 2011 representing 30 per cent of Middle East totals. By end-2012 there is expected to be 23Mta of excess capacity with Saudi Arabian demand closing the gap. Going forward, utilisation rates are forecast to stabilise, according to GIH estimates, as only a few new companies are set to come on-line. In terms of the business environment, M&A activity has picked up very strongly since the financial crisis, with the UAE being the main hot spot. Vertical integration is also being seen as a way forward.

The East African cement industry remains on a steady growth path and Francis Mwangi of Standard Bank, Kenya presented a detailed paper on the market’s strong fundamentals as well its challenges. Government infrastructure spend across the region is increasing and a boom in the private construction sector is being driven by rising housing demand and an expanding middle-income population. Building of commercial property is also on an upward trend as economic growth drives the creation of new cities. As such, cement demand currently stands at 7.6Mt.

Meanwhile, cement capacity has increased by 68 per cent over the past five years to 10.6Mta. Further rises of 40 per cent to 14.8Mta are expected by 2015 with Kenya accounting for 51 per cent. The structure of the East African cement production base has also seen changes over recent years. Traditionally dominated by multinationals, since 2008 capacity additions have mainly been driven by new local entrants and this fragmentation is expected to translate into increased competition. However, it is the lack of new clinker capacity that remains the region’s “wild card,” Mr Mwangi observed, as no significant investments have been made over the past 10 years. With quality and mapping of limestone deposits a major challenge, new players are mainly establishing grinding lines with plans to import clinker. Imported clinker, he noted, is 30-50 per cent higher than locally-produced volumes.

Turning to the Egyptian market, Ahmed Abu Hussein of Cairo Financial Holding (CFH) explained why, after an unsettling 2011, the local cement sector could be on the brink of a strong rebound. While political uprisings created a challenging operating environment, Mr Hussein believes that once the country’s political framework is reformed (expected to be completed by mid-2012), economic confidence will be restored and construction will be one of the first sectors to rebound. This bodes well for the cement industry which last year saw demand fall 1.7 per cent as 6Mta of new capacity came online. Over 2012-13 some 12.4Mt of capacity is scheduled to come on-stream and 12 new licences could be offered. Nevertheless, Mr Hussein stresses that given Egypt’s immense infrastructure and housing needs and a large population base, “the market will definitely need more capacities as demand is forecast to exceed new capacity additions.” He added that the reconstruction of Libya also presents a major opportunity for the Egyptian cement sector.

Ahmed Nader of Al Maysarah Co, Jordan

Another country teeming with potential is Iraq, as outlined in a presentation by Ahmed Nader of the Al Maysarah Group, Jordan, whose company is involved in three regeneration projects in the west. As the country looks to rebuild following decades of war and uncertainty, there is currently a massive drive towards refurbishing old cement plants and constructing new facilities. Of the 25.5Mta of total planned cement capacity in Iraq, some 60 per cent (15.4Mta) will be situated in the west of the country. The Al Maysarah Group projects include:

• Al Qaim Cement plant (one line, 1Mta design capacity). Rehabilitation started in March 2009, followed by an optimisation project, resulting in a constant high-quality production increase to 3400tpd of Sulphate-Resistant Cement

• Kubaisa Cement plant (two lines with a design capacity of 1Mta each). Rehabilitation of Line 1 started in October 2010 and will be followed by an optimisation project. Work on Line 2 began in October 2011 and 65 per cent has been achieved. The target results are a constant production increase of up to 3400tpd of OPC each (ie, a total of 6800tpd or 2.2Mta)

• Falluja Cement plant (three lines with a total capacity of 290,000tpa). To date, 9MW power plants have been installed and options are now being studied to rehabilitate the wet-process line, upgrade one dry line and convert the other to produce oil well cement.

Hatsey Berhe of Messebo Cement, Ethiopia, outlines the

development strategy for the local cement sector

As Ethiopia goes through a transitional phase, Hatsey Berhe of Messebo Cement Co then explained to delegates how the local cement sector is also set to be a key beneficiary of a new government development strategy. The Five Year Growth and Transformation Plan (FY10/11-FY14/15) will provide supportive measures to raise production capacity from 13Mta (as at June 2012) to 27Mta by 2015 and achieve per capita demand of 300kg by the end of the planned period.

Further updates on new African cement projects came in the form of Dangote Cement’s breath-taking multibillion dollar investment drive. The Nigerian producer is targeting 50Mt by the second half of 2014 as it expands its three domestic facilities as well as constructing integrated cement plants in Ethiopia, South Africa, Senegal, Zambia, Tanzania and Gabon. In addition, the group is constructing a new grinding unit in Cameroon plus a number of terminals in various African countries. It is also keeping a keen eye on the markets of Egypt, Mozambique and Kenya and says it has been short listed for a government licence in Algeria.

The niche market of white cement was reviewed by Chris Blasdale author of ICR's recently-published Global White Cement Report Second Edition. Analysis shows that the Middle East has experienced the strongest growth worldwide in white cement consumption over the 2002-10 period (up 9.1 per cent annually). Going forward, it is expected to grow at a CAGR of six per cent over 2010-15 period, accounting for 18 per cent of total global market share. Meanwhile, Africa, excluding Mediterranean North African countries, remains a very low consumer of white cement (0.23Mt in 2010), barely over one per cent of the global market. Forecasts put growth rates at a CAGR of six per cent between 2010-15.

Technically-speaking...

Kalyan Bose of Yanbu Cement, Saudi Arabia,

on the company's new 10,000tpd line

Case studies and a broad range of technical papers provided practical advice for producers competing in today’s modern cement industry.

Kalyan Bose of Yanbu Cement, Saudi Arabia, provided an interesting overview of the company’s new 10,000tpd line No 5, the main contract for which was awarded to Sinoma of China. The project scope encompasses raw material crushing right through to bulk and bag cement packing. Major equipment was supplied from Europe and China.

Raw materials came under the spotlight with presentations by Simon Turner of Stevin Rock LLC who explained quality control of cement kiln feedstock from a limestone producer’s perspective. Sebastian Müller of ABB then gave an example of analysing limestone using near-infrared technology at a project completed for Raysut Cement, Oman.

A technical session dedicated to alternative fuels

technology and waste heat recovery solutions

As cement producers worldwide look to explore plant efficiency with increased vigour, alternative fuels and waste heat recovery systems (WHR) formed a key part of the agenda. Presentations were delivered by Karl Menzel on the Vecoplan FuelTrack approach to treatment and handling of alternative fuels technology, and Luc Rieffel of the ATS Group talked delegates through the successful application of waste solid fuels in Asia and Africa. Following on, Virendra K Batra of Holtec Consulting, India, then demonstrated why WHR power plants are becoming an integral part of combined operations and explained the imperatives of customising WHR solutions.

Under the theme of grinding technology, Dr York Reichardt of Gebr Pfeiffer discussed some of the company’s latest advances in vertical roller mill technology, highlighting recent project completions and newly-awarded contracts such as the world’s largest vertical roller mill for Holcim (Brasil). Mohammad Khoozestani of Namadin Sanat Iran then discussed process control for optimising grinding performance in ball mills achieving 5-25 per cent increases in milling capacity with the same percentage in energy savings.

Other aspects of cement manufacturing explored included the latest bagging advances from Haver & Boecker, high-efficiency clinker cooling by Fons Technology International and a case study of an ESP bag filter conversion at Holcim Lagerdorf, Germany, by Scheuch.

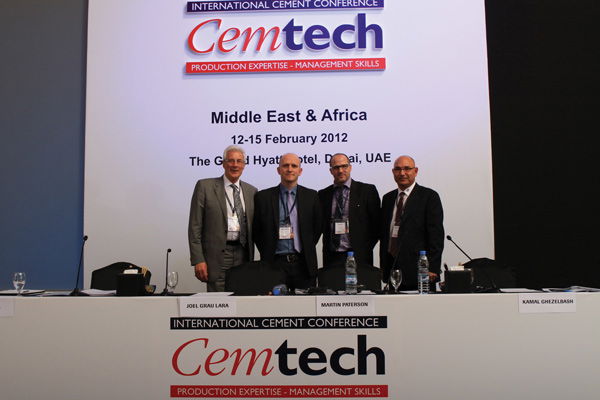

The shipping news: a session dedicated to freight markets

and cement terminal technology proved highly informative

A session focussing on shipping markets and technology proved highly popular with Joel Grau Lara of Clarksons leading the way with forecasts on dry bulk freight fundamentals. Here he observed that strong fleet growth will continue during 2012 which will put freight rates under pressure. Demand for drybulk commodities are expected to be strong and grow by six per cent this year.

From a technical perspective, Martin Paterson of IBAU Hamburg described import terminal projects undertaken by the company at a number of European operations. Pneumatic conveying systems by Claudius Peters were later discussed by Kamal Ghezelbash, namely the company’s Fluidcon system, which has 75 references worldwide.

Exhibition arena

An international exhibition provided

an additional networking area

A bustling international exhibition, held alongside the main conference, showcased the latest technology advances and services, providing an informal platform to create and develop commercial relationships.

Workshop and plant visit

A technical workshop, led by Michael Clark of e-Learning, looked at the cement kiln mass balance, clinker quality and emissions, providing plant managers, process engineers and technical personnel the opportunity to develop an advanced understanding of modern cement manufacturing practices.

Cemtech plant tour to Fujairah Cement

Delegates also had the opportunity to tour the recently-expanded Fujairah Cement Works, one of the most advanced cement operations in the Middle East. Located in the small town of Dibba, the company’s new 7500tpd line, supplied by Polysius was the highlight of the tour, showcasing state-of-the-art technology in action. Constructed parallel to the existing cement plant, the new line has been producing cement since 2010.

Unbeatable hospitality

An open air Gala Dinner filled with live entertainment

concludes proceedings in tru Cemtech style

Cocktail receptions, superb three-course lunches and dinners and a partners’ programme touring some of Dubai’s traditional and modern attractions, all combined to make this Cemtech meeting a thoroughly memorable event. To conclude proceedings with a final flourish, delegates were treated to a Gala Dinner under the Dubai night-sky filled with fine food and entertainment featuring magic shows, acrobatic displays and live music.

With Cemtech Middle East and Africa now successfully completed, plans for next year’s event are underway. In the meantime, we turn our attention to Cemtech Asia 2012, taking place in Jakarta, Indonesia, on 17-20 June 2012. Focussing on the high-growth markets of the Asia and Asean region the meeting looks set to be another busy event. We hope to see you there!

This article was first published in the April 2012 issue of International Cement Review