Cem Prospects 2016 gathered together cement producers, solid fuel traders, suppliers and freight specialists for a two-day conference exploring the energy markets and outlook for the year ahead. Held at the Hilton Athens, Greece, on 6-8 November, the meeting was organised by Cimeurope sarl, a subsidiary of CEMBUREAU – the European cement association.

Cem Prospects' meeting was held at the Hilton Athens, Greece on 6-8 November, and was organised

by Cimeurope sarl, a subsidiary of CEMBUREAU – the European cement association

The conference provided a forum for cement producers to explore the global energy markets, with a particularly emphasis on primarily fuels, including coal and petcoke.

Chairman of the conference, Patrick Peenaert of AGP Traco (Switzerland) and formerly Lafarge (France), stressed the need to take note of the increasing societal and regulatory pressures for the energy sector in the wake of the COP21 meeting in Paris.

The first morning of presentations saw detailed presentations on the cement industry. Koen Coppenholle, CEO of CEMBUREAU, provided an overview of the cement industry in Europe, which accounts for 5.5 per cent of global cement production (4.6bnt) in 2015.

From a fuel perspective, Europe’s cement producers have now reached around 41 per cent alternative fuel substitution, replacing the equivalent of 6.5Mta coal, reducing CO2 emissions by 16Mta. However, the industry will have to respond to the rising pressure of climate change, including reaching increasingly-tight targets through new levels of innovation. This will inevitably impact solid fuel consumption in the long run.

Climate challenges in the transport sector, especially shipping, will also impact on the cost of freight, while the impact of regulation on supply, for example sulphur restrictions on petcoke, also need to be considered, argued Mr Coppenholle.

Dr Vagner Maringolo, Environment & Resource Manager for CEMBUREAU, pointed out the large potential for co-processing waste in cement plants to go well beyond current levels. The availability of combustible waste in the EU is measured at 530Mt. EU cement plants have no technical limitation on their ability to increase alternative fuel substitution from the current level of 36 per cent (consuming 9.8Mt waste) to 60 per cent (18Mt waste), while incurring negligible investment costs. By comparison, to achieve the equivalent with energy-recovery incineration (ie waste-to-energy incinerators) would require an investment of between EUR8.6bn-15.6bn. Yet significant barriers to achieving this target exists from a lack of waste collection and processing infrastructure, as well as political and regulatory barriers. Alternative fuel substitution levels of 95 per cent are technically feasible but would require very significant levels of investment.

Global coal markets rally following cuts to Chinese production

Recent trends in the coal market and the outlook for 2017 were the primary focus for the next session of the day. Frank Brannvoll, manager Energy, Economic Studies & Statistics for CEMBUREAU, provided a comprehensive overview of coal prices and related fuels in the energy markets.

Crude oil prices, which collapsed as a result of Gulf oil producers' failed attempt to flush out shale production in the US, are seen trading in the range of USD42-55, with the outlook nudging up towards a range of USD55-65 for 2017 if OPEC producers follow through on their plans to cut production to tighten supply and strengthen prices. (Indeed, since the event concluded, crude oil rose to 16-month high of US$55 a barrel on 30 November following OPEC’s deal to cut production.)

Frank Brannvoll took over from Sven Rydahl as the editor of

Cimeurope’s Cemreview publication. Published every 6-8 weeks,

the report produces analysis and forecasts for energy prices (crude oil,

natural gas, steam coal, petcoke) as well as commentary on freight

rates and the carbon market.

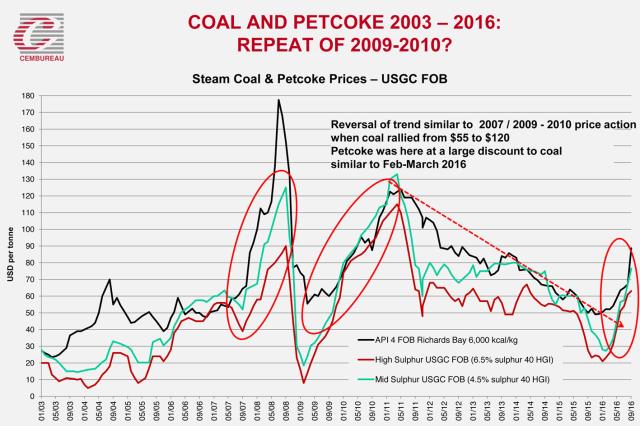

Coal prices have experienced a particularly volatile year to date. In the first half of 2016, the long-term support price of US$40/t for steam coal held as prices reached the bottom of the current cycle in March before rising steadily. Since October, however, steam coal prices rallied, rising to in excess of US$100/t, and decoupled from oil in the process. This followed the reduction in supply as China surprised the market by reducing the working days in mines to 276 from 330 and bad weather impacted production in Australia and Indonesia.

According to Frank Brannvoll, API 4 FOB Richards Bay is seen trading at an average of US$95/t in the short term but stabilising at around US$75/t in 2017 as Chinese production returns. For API2 coal, prices are will range between US$60-80/t over 2017, with an average price of US$70/t.

Having set the scene, a panel coal consultants, buyers and traders discussed the outlook for coal prices in greater detail. Guillaume Perret, Perret Associates (UK) warned that coal prices could rise much further due to a combination of historically-low coal stocks (down 50Mt lower since the start of 2016), unprecedented cuts in production (down to 162Mt in the USA – the lowest level since 1978), lack of new coal mines coming on-stream, and a potentially harsh winter intensifying demand as supply drops.

Source: CEMBUREAU

Xavier de Vos, coal trader for Engie (Belgium), commented on his concerns with regards to forecasting prices, arguing that the main indexes are based on a narrow part of the market and are therefore not representative. In his view, it is better to combine any market outlook with a methodology that looks at the fundamentals of supply and demand.

Freight market developments

The second day of the conference commenced with a session on freight market developments led by Simon Cox, a dry bulk specialist at Howe Robinson (UK). Simon provided a masterclass on freight transportation, exploring the fundamentals of vessel utilisation in the various carrier classes that have seen the index climb modestly in 2016 from an all time low at the start of the year. In the near term outlook and over the coming 12-18 months, freight rates are likely to remain broadly in the band they are in now. Looking ahead, fleet decline due to a lack of investment in new capacity will see utilisation rise and prices will strengthen.

Source: CEMBUREAU

Petcoke markets

All petcoke grades have risen higher, observed Frank Brannvoll, driven by the sharp rally in coal. Higher coal prices have incentivised users to switch to petcoke, which has in turn caused prices to rise to US$76.5/t for medium-sulphur (USGC FOB 4.5 per cent and US$63/t for high-sulphur coal (USGC FOB 6.5 per cent). In addition, increased demand was apparent as Indian buyers (notably in the cement sector) were seen entering the market, with imports surging massively for both mid- and high-sulphur grades of the fuel, explained Frank Brannvoll.

Prices also rose due to supply side constraints, including a reduction in USGC mid-high sulphur production and a drastic reduction in Venezuelan exports, creating scarcity in the mid sulphur grades.

Petcoke is traded at a discount to coal, which at the start of the year was in excess of 60 per cent versus FOB prices, and has since reverted to the ‘neutral’ zone of around 40 per cent.

Looking forward, Mr Brannvoll argued that the market was moving from sellers to buyers market. Prices for high-sulphur product will range between US$60-70/t, stabilising from current higher levels at around US$80. Low-sulphur coal (4.5 per cent USGC) is seen in the US$70-80/t range.

Following Mr Brannvoll’s detailed overview of recent market trends, an expert panel discussion debated various scenarios for the year ahead. Lars Schernikau of HMS Bergbau (Singapore) warned of further competition for petcoke from the power sector and noted that India may ban high-sulphur petcoke, potentially increasing costs for domestic cement producers.

Gonzalo Solis, representing Repsol, argued that Africa was the region to watch out for going forward and would be the main driver of prices in the longer term.

Another participant pointed out that the world trade in petcoke amounts to around 50Mta, with the US producing and exporting around half of this volume. As petcoke cannot be stored for lengthy periods, it must be sold, meaning stocks are limited. Consequently, one individual consumer can take up all surplus stocks in one go and disproportionately impact the global market. This makes forecasting prices complex, a process that is not made easier by the fact that there is a lack of transparency in the sector and no reliable index to benchmark the market. Something that stakeholders may seek to develop going forward.

Cemprospects offers a unique industry forum for the discussion of all energy- and fuel-related topics and is an essential meeting for all involved in buying fuels for cement facilities.