The Baltic Dry Index reflected the trends in the handy and capesize markets as it rose from 1103 to 1146 on 11 July, but then slipped to 1074 one week later.

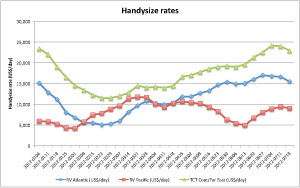

After a stable week ended 11 July, the handysize market experienced a softening the following week, particularly in the Atlantic Basin where day rates fell from US$16,600 to US$15,447 for the RV Atlantic contract on 18 July. The Pacific counterpart noted a four per cent drop from US$9400 to US$9000. Few new cargoes were observed as the summer lull is upon the sector.

After a stable week ended 11 July, the handysize market experienced a softening the following week, particularly in the Atlantic Basin where day rates fell from US$16,600 to US$15,447 for the RV Atlantic contract on 18 July. The Pacific counterpart noted a four per cent drop from US$9400 to US$9000. Few new cargoes were observed as the summer lull is upon the sector.

Customers wanting to charter a panamax-sized vessel would face a more expensive bill during this period as RV rates advanced by 13.5 per cent to US$10,500/day on transatlantic contracts and 11.3 per cent to US$8350/day on TCT Far East journeys on 11 July. The subsequent week saw again modest increases – this time by 3.8 per cent to US$10,900/day and 4.2 per cent to US$8700/day, respectively. Fresh coal cargos on the Atlantic were noted by Fearnleys, but a surplus of tonnage remains, subduing price levels.

The capesize market lost its 10 per cent advance gained in the week ended 11 July one week later. TCT Cont/Far East rates returned to a more modest level of US$23,200/day after peaking at US$25,900. Meanwhile, the tonnage rate for Richards Bay-Rotterdam dropped to US$6.45 on 18 July after rising to US$6.70 the previous week.