2021 has seen the dramatic rebalancing and recovery of global cement markets, the majority of which have made up for ground lost to the pandemic in 2020.

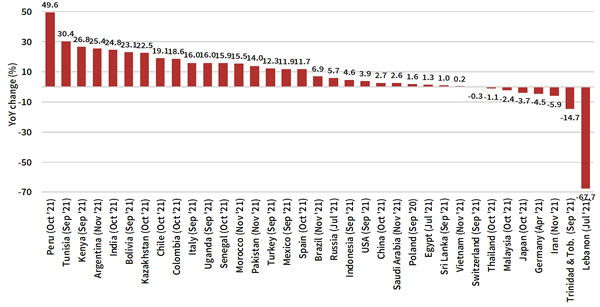

Among the largest markets, India is seeing a recovery in rural housing projects, which alongside a good monsoon season and a pick-up in infrastructure projects has strengthened cement demand, with YoY growth on track for 25 per cent in 2021. The USA is also seeing progression in market recovery despite the adverse impact of weather in the 1H21, as underlying demand and the US$1.2tn infrastructure bill provide hope for future demand. Other large markets are also seeing sustained demand, with Brazil and Russia expected to reach positive growth of 6-7 per cent in 2021.

Africa was a particularly bright spot in 2021, with Kenya, Uganda, Senegal, Morocco and Tunisia all seeing supercharged growth at high double-digit levels. On the other hand, weaker trends were observed in Asia where the pandemic’s resurgence has triggered lockdowns that are stifling the economic recovery. The ASEAN markets suffered negative growth rates, while the pace of growth slowed to 2-3 per cent in China against a difficult economic backdrop and the real estate crisis.

YTD cement volume change, compared with previous year (as reported Dec '21)

Sustainability and cost concerns

Certainly, one of the most significant events of the year was the move towards tighter sustainability targets. As COP26 was held in October-November, the industry’s main players and largest associations all announced their respective ambitions towards 2030 and beyond. With producers announcing net-zero emissions targets for their entire value chains by 2050, attention also turned to the technology that can make this a reality. Carbon capture and utilisation (CCUS) is one such important tool, with HeidelbergCement setting out a target to reduce CO2 emissions by 10Mt by 2030 through the use of CCUS.

In addition, a growing concern in Europe is the rising price of carbon that may reach EUR100/t by the end of the year after posting a 50 per cent increase since the start of November. The rise in prices has been attributed to a surge in coal usage, raising demand for carbon allowances, amid gas supply concerns.

This is only one segment in the overall cost inflation for cement producers, with energy, freight and distribution costs also seeing a considerable uptick. The previously-noted supply concerns regarding natural gas pushed prices for the fuel upwards, leading to many consumers switching to coal and therefore pushing prices for this material up at the same time. The rise in coal and gas prices, alongside the resulting high carbon prices, has had a similar effect on electricity prices. The global energy supply deficit was also taking place alongside a surge in freight rates during the year, partially attributed to COVID-19 protocols at key ports causing bottlenecking and demand for ships outstripping supply.

Producers have been combatting the rise in costs with mostly successful price increase programmes. Cemex implemented a second round of price increases in the US to cover its cement and ready-mix businesses over the third quarter, which saw prices rise two per cent sequentially, but it was still not enough to offset rising energy and input costs. HeidelbergCement also announced a business excellence programme to combat the ongoing cost inflation, which is expected to reduce cost inflation by at least EUR500m by the end of 2022.

Outlook for 2022

Looking ahead, producers are hoping that the positive signs for underlying cement demand offset cost inflation into next year. However, the threat of new COVID-19 variants remain and the prospect of further lockdowns are a possibility, especially in Europe. Therefore, cement price increases to ease the pressure on margins are expected to continue. While this may be enough for producers with domestic capacity, importers will struggle with the double threat of cost inflation and surging freight rates.

Finally, the progress made towards the industry’s sustainability ambitions this year will need to continue in 2022, alongside a focus on the technology that will help it meet them, with clinker reduction and alternative fuels front and centre.