Iranian cement producers are under pressure from weak private demand at home and strong competition in export markets. Weakening economic growth, double-digit inflation and tight monetary policy have hit private construction activity in Iran hard. The residential property market has stagnated after unsustainable price rises and slumping demand.

Moreover, it was reported in the Iranian media this week that cement and steel plants have been ordered by the government to suspend all operations for a 15-day period, effective from 15 May, to control demand for electricity. The measure, which Iran’s Association of Cement Producers has unsurprisingly warned will harm output across the industry, is being attributed in part to record temperatures leading to increased use of domestic air conditioning systems and placing a burden on electricity supply. The situation is expected to improve in mid-June after power plant repairs have been completed.

Public infrastructure remains the key bolster of construction and cement demand in the country. Although the government is promising substantial infrastructure projects, any further revenue shortfall, such as that recorded in 2023 due to oil and gas revenues taking a hit from economic sanctions, is a threat to such investment. Additionally, with China and Russia the main source of foreign investment in Iran’s building and infrastructure sector, difficulties in these countries could destabilise some long-standing projects and may limit further investments into the Iranian construction sector.

Economic sanctions are also increasing the cost of machinery and restricting financing which combined with fuel shortages and power outages are adding to Iranian cement producers concerns. The country has a total nominal capacity of 109.552Mta of cement, 99.852Mta of clinker, and an additional 2.991Mta of white cement, distributed over 94 facilities, of which two thirds are government-owned.

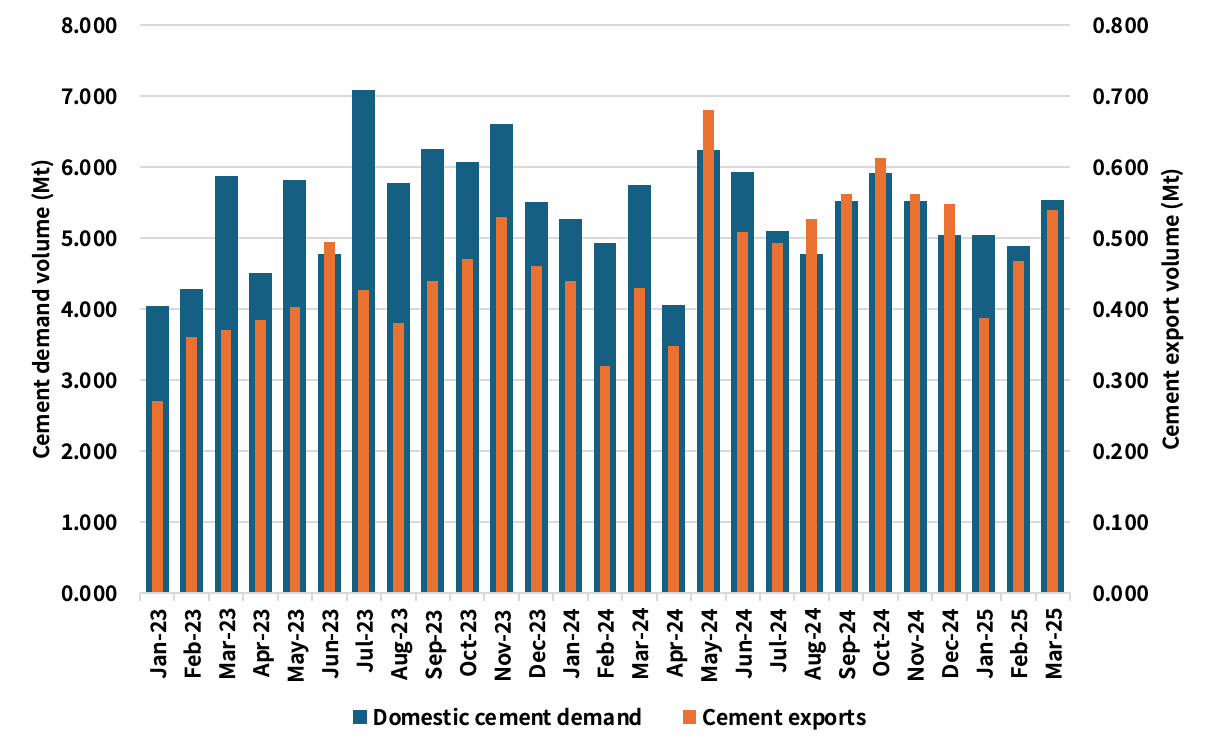

The latest data from the Iranian cement association shows domestic demand fell 3.1 per cent YoY in the first quarter of 2025, coming in at 15.461Mt. Meanwhile, cement production increased just 1.1 per cent YoY to 16.72Mt and clinker production was 16.951Mt, up 2.2 per cent YoY. Cement exports amounted to 1.393Mt in the 1Q25, up 17.1 per cent YoY, while clinker exports were down 36.3 per cent YoY to 1.402Mt.

The Iranian FY24-25, which runs from 21 March 2024 to 20 March 2025, shows domestic cement consumption in Iran amounted to 63.558Mt, a fall of four per cent YoY, with cement production down 2.1 per cent YoY to 69.966Mt, clinker production down 6.9 per cent YoY to 71.387Mt and clinker exports down 34.8 per cent YoY to 5.825Mt. Cement exports alone noted an increase, rising 18.3 per cent YoY to 6.235Mt.

While Iran remains one of the most important cement and clinker exporters globally, it is facing increasing competition, in particular from Egypt. Although Iran maintained its position as the fourth most important cement exporter globally in 2024, helped by the Iranian rial’s depreciation, Egypt, benefitting from its own currency devaluation, jumped to third from eighth position, with an increase in exports of over 4Mt to 7.6Mt. China also rose notably in the rankings with a 1.4Mt jump in cement exports to 4.6Mt during the year. Kuwait, Afghanistan and Russia are Iran’s key cement export markets.

At the same time, Iran slipped to sixth place in 2024 from fifth place in 2023 in global clinker exports ranking as other countries in the top 10 increased their exports by on average 1Mt during the year, while Iran’s fell notably. Egyptian clinker exports jumped by 2.4Mt to 12.2Mt. Clinker exports from Iran to previously key markets, India, Bangladesh and Sri Lanka, have fallen off sharply in recent years with the countries adhering to UN-backed sanctions. Iraq and Kuwait account for around three-quarters of clinker exports. Iranian government-owned Fars and Khuzestan Cement Holding has a 0.8Mta grinding facility in Maysan in Iraq.

Competition and limited opportunities to enter new markets may see Iran slip further down export rankings in 2025, and while renewed impetus on infrastructure construction will help revive domestic cement demand during the year, the risks are weighted to the downside.

Figure 1: Domestic Iranian cement demand and export volumes, Jan 2023-Mar 2025