By Frank O Brannvoll, Cimeurope sarl, Belgium

Last month the US$/EUR trading range was set at €1.04-1.08 and has held within €1.05-1.075 at €1.0720. Other than the US Federal Reserve Bank raising its overnight rate by 0.25 per cent to one per cent, there is no other major news. The increase did not have an impact on the US$/EUR rate with the expected range going forward between €1.05-1.10.

Crude oil

Crude oil price developments can often be considered as a front runner for overall energy price developments.

The market has remained confined within an uptrend channel since 1Q16, starting from below US$30/bbl. Over the past year, this channel has defined the highs and lows of Brent Crude oil. The OPEC agreement in December sent oil above the crucial US$53.30/bbl resistance level, based on expectations that production cuts would now balance supply and demand. Oil hit US$58, with major financial positions subsequently going long in the market in anticipation of even higher prices of US$60-65 (the top of the trend channel). However, output has also increased in countries such as the US with current prices supporting US shale producers to sell at above break-even points. Since the agreemnt, more US rigs are being added every week, taking rig numbers from a low 404 in 2Q16 to a current 768. Moreover, new data show increasing oil stocks despite the agreement and Saudi Arabia lifting its output. This has resulted in oil prices falling below the current key support point of US$53.50. The market reacted by testing at US$50.50 – down to the trend line.

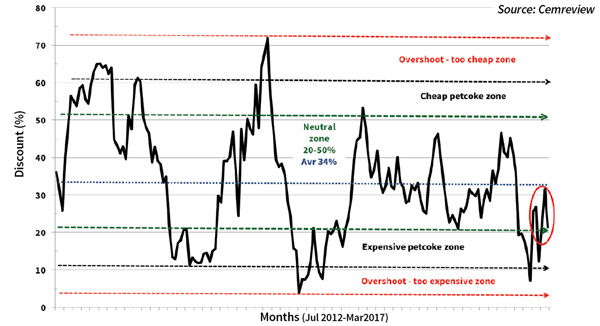

Figure 1: petcoke discount to coal petcoke discount to coal (API 2 USGC6.5% cfr ARA 6000kcal base – March: 21%)

The OPEC agreement will only run until June 2017 with no current indications of an extension. To keep oil prices within an uptrend, it is crucial that this level holds, otherwise several stop loss orders could be executed in long positions. Without any new fundamental supportive news, a new direction could be recorded, with an initial target of US$46. However, producers are verbally indicating support, and on the daily chart oil is oversold. An initial reaction would be to revert back to the major US$53.50 pivot point.

Looking ahead, a range of US$50.50-54 is forecast. Any fall below US$50 merits close monitoring as this could set the energy trend for the coming months.

Coal

Eyes remain on China as the NRDC plans to reintroduce new domestic production cuts, and has already introduced preferred price ranges for domestic coal. These new measures are not perceived as being as harsh as the former restrictions and target capacity (rather than direct production cuts) up to 150Mt, culling the least efficient mines. In addition to reducing pollution, the capacity cuts are designed to insulate power and coal producers from a repeat of the sharp price increases seen in 3Q and 4Q16. The market has reacted calmly with slight price increases above CNY600/t to reflect a short-term physical supply issue.

Front-month API 4 FOB prices have fallen from US$83 last month to US$78. With the warmer season in place we may see a test of US$72, depending on whether oil will fall below US$50/bbl. The front year still trades within its uptrend channel from April 2016 having support at US$70/t, apparently stabilising between US$65-75/t. Forecast ranges for front-month and front-year prices are US$72-82/t and US$70-75/t.

Petcoke

Petcoke prices (USGC FOB – 4.5 per cent and 6.5 per cent sulphur, both 40 HGI) are tracked and analysed by Cimeurope using different methodologies.

Since March, a 10 per cent increase was noted in the petcoke prices and a relatively lower discount to coal is taking place (see Figure 1). ARA API 4 fell from 35 per cent in February to 21 per cent currently. Approaching the expensive petcoke range, the market is closely watching some potential big fundamental drivers. A key driver is India, where the banning of petcoke use in the NCR of Delhi, as well as nationally, has been discussed. However, cement producers have a certification for continued petcoke usage, even in the event of such a ban. Nevertheless a ban would considerably impact demand and price levels.

Petcoke imports have also been affected by increased freight costs, up 25-50 per cent in the last month following January-February lows.

At this time of year Indian demand is expected to pick up, and as the effects of the demonetisation are fading out, the cement sector demand should normalise.

Depending on the development of coal, Cimeurope expects the discount to widen again toward 30 per cent, leaving room for “less expensive” coal. USGC-ARA freight costs are estimated at US$17/t.

|

Prices at a glance |

|

|

Crude oil - bbl |

US$52.50 |

|

Coal API 4 - April |

US$78.25 |

|

Coal API 4 - Cal 2018 |

US$71.00 |

|

Petcoke |

|

|

USGC 4.5% USGC 40HGI FOB |

US$68.00 |

|

USGC 4.5% USGC 40HGI cf ARA |

US$85.00 |

|

USGC 6.5% USGC 40HGI FOB |

US$55.50 |

|

USGC 6.5% USGC 40HGI cf ARA |

US$72.50 |

Price-related terminology used in the text (eg support, resistance, trendlines, objectives, targets, cheap and expensive) should be understood as technical financial terms commonly used in market analysis.

The author is Editor of CEMREVIEW, published by Cimeurope SARL (cimeurope@cimeurope.eu).