By Frank O. Brannvoll, Brannvoll ApS, Denmark

The euro was stable between US$1.12-1.14 despite the US Federal Reserve focussing on higher yields in 2022. A range of US$1.12-1.16 can be expected in the next few months, still looking towards US$1.18 later in the year.

The Turkish lira collapsed to TRY18.40, before new strict curbs forced it back to TRY10.50. Still under pressure from negative real interest, the lira has softened to TRY13.80.

|

Table 1: Prices at a glance |

||

|

Crude oil (US$/bbl) |

81.75 |

|

|

Coal |

API2 – 1Q22 (US$) |

132.00 |

|

API2 – Cal 2023 (US$) |

97.00 |

|

|

API4 – 1Q22 (US$) |

141.50 |

|

|

API4 – Cal 2023 (US$) |

96.00 |

|

|

Petcoke |

USGC 4.5% 40 HGI – FOB (US$) |

142.00 |

|

|

USGC 4.5% 40 HGI – CFR ARA (US$) |

168.00 |

|

|

USGC 6.5% 40 HGI – FOB (US$) |

121.00 |

|

|

USGC 6.5% 40 HGI – CFR ARA (US$) |

147.00 |

Coal and gas

The oil market was supported by COVID-19’s latest variant, Omicron, not causing extensive lockdowns, and political turmoil in Kazakhstan that is threatening its oil exports. However, the Kazakh authorities have been supported by Russian intervention and the risk premium for oil could fade.

The gas market is rising as Russia is delivering only contractual amounts. This is a political powerplay on the Nord Stream 2 pipeline project to be approved in Germany.

OPEC+ kept the steady course on lifting only 0.4mbpd at its January meeting. In terms of the next meeting on 2 February, there are also low expectations for further increase. Meanwhile, the situation at the Ukrainian border is still adding a risk premium to oil.

The Brent oil price rose eight per cent to US$81.75, returning to an uptrend. Resistance is at US$82.50 and US$86, with support increased to US$80 and US$76 – the long-term support at US$67. Brannvoll ApS sees a US$60-100 range with an average of US$75 in 2022.

Coal

Coal dominated with news from Indonesia and China. China’s domestic production increased sharply and the Chinese domestic price fell to CNY700 (US$96), down from CNY1180 in November. Further Chinese curbs to reduce pollution during the Olympic Games also put pressure on prices. In Indonesia a sharp decrease in production has led to the country’s government banning exports in January, removing almost 40Mtpm from the Pacific market, which sent Australian and South African coal upwards. Europe is still increasing its coal demand due to the downtime of French nuclear reactors in addition to coal remaining the cheapest power fuel despite CO2 prices at €85.

The API2 front-quarter (1Q22) contract rose two per cent to US$132. Support is at US$120 and US$110 with resistance at US$150 and US$175. The API2 new front-year Cal23 contract started at US$97, 15 per cent lower than Cal22 ended. Support is at US$90 and US$87 while resistance is found at US$102 and US$110. The expected range is between US$90-105.

The API4 front-quarter (1Q22) rose 11 per cent to US$141, with support still at US$125 and US$110. Resistance is at US$150 and US$160. The API4 new front-year Cal23 contract started 17 per cent lower than Cal22 at US$96, with support at US$92 and US$85. Resistance is at US$102 and US$120. The expected range is between US$90-105.

Petcoke

Petcoke trading was very thin with limited deals at the end of the year as big spreads between buyers and sellers were seen.

Refiners in India were active in the export market as domestic demand is still low. They are increasingly offering lower prices to see the petcoke flow. However, the increase in coal prices as well as lower freight prices did support FOB pricing.

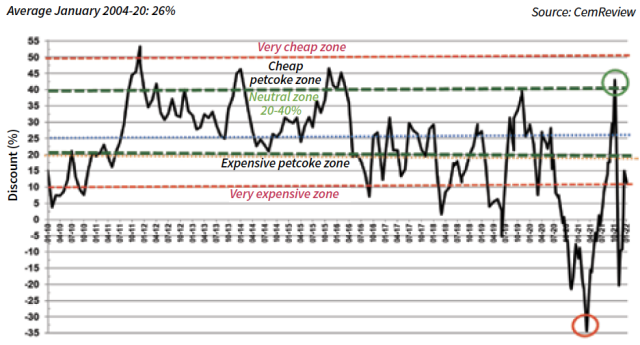

Petcoke discount to coal – API2 USGC6.5% ARA based on 6000kcal, Jan 2022: -11%

The overall drivers are still gas and coal prices. In the case of Turkey, the value of the lira will also have an effect.

However, one loading terminal in Houston, USA, is down and has the potential to disrupt shipping for some time although only with limited effect.

The discounts on FOB are positive and are expected with this high energy complex to attract buyers back to petcoke. However, falling Chinese coal prices keep buyers reluctant as the impact from the Indonesian export ban may come to a halt by the end of January.

The USGC FOB 6.5 per cent sulphur (S) contract fell three per cent to US$121 with the discount to API4 up from 21 to 31 per cent. A range between US$115-130 is now forecast. The ARA contract price fell eight per cent to US$147 and the discount increased to 11 per cent – still in the expensive zone.

The USGC FOB 4.5 per cent S contract rose two per cent to US$142 with a 11 per cent discount. A range of US$125-150 can be expected. The ARA rate of US$168 is lower due to a fall in the freight rate but remains at a premium of two per cent to API2.

The spread between 4.5 and 6.5 per cent S petcoke further widened above the normal US$4-6 to US$21 and is expected to stay in the range of US$10-25 as demand for the medium is less able to substitute.