The global markets went into turmoil after the US administration declared the new custom tariffs and their size. Presently, the impact on stock markets and the potential influence on global demand remains unknown. The Volatility Index (VIX) rallied from 20 to 60, levels not seen since COVID-19. Its impact on the commodity markets reflects the fear of a fall in demand and the overall complex has gone lower. To make short-term predictions at this stage is almost like betting, since a few words or changes to the US decrees may turn the picture upside down. On the broader geopolitical stage, Ukraine-Russia ceasefire talks are dragging out with the war continuing.

The time for central banks to respond, potentially by lowering interest rates is coming closer, but at the same time US tariffs could drive inflation higher. In March the ECB cut its interest rate by 0.25 per cent to 2.5 per cent, while the US Federal Reserve kept its range unchanged, awaiting the full impact. The US dollar has fallen both on the broad US$ index by six per cent and against the euro. It is currently testing resistance at US$1.10, with a higher range of US$1.07-1.1250 expected. Brannvoll ApS forecasts a range of US$1.05-1.15 in 2025, with an average of US$1.12.

| PRICES AT A GLANCE - 5 May 2025 | ||

| Brent crude oil – bbl | US$60.00 | |

| Coal API 2 | 3Q25 | US$98.00 |

| Cal 2026 | US$106.00 | |

| Coal API 4 | 3Q25 | US$91.00 |

| Cal 2026 | US$103.00 | |

| Petcoke USGC 4.5 per cent S 40HGI | FOB | US$72.50 |

| CFR ARA | US$89.00 | |

| Petcoke USGC 6.5 per cent S 40HGI | FOB | US$67.50 |

| CFR ARA | US$84.00 | |

Oil

This month has seen another fall in the energy complex, driven in particular by demand fear in the oil market and the fact that OPEC+ seems determined to increase production despite the price being below US$70 – a pain threshold the market expects OPEC+ to defend. US production is at a record high, and if sanctions on Russia were lifted, Russian oil could hit the market as well, outweighing the impact of potential sanctions on Iranian and Venezuelan exports. The market outlook for the next weeks will likely be most on the downside until the effects of tariffs become clearer.

TTF gas prices also fell back, sending Cal26 back to US$39 levels, with the EU looking to replenish its low stocks. Brannvoll ApS forecasts a trading range of US$65-90 and average of US$75 for 2025.

Coal

The coal market, which had already fallen in previous months, maintained price levels despite ample supply. Chinese and Indian production increased while their domestic prices fell and stock levels were high at Chinese ports. Falling demand from Japan, Taiwan and South Korea has seen Newcastle coal falling to US$100. Russian producers are selling below production cost, and there are new closures of Russian and Australian mines.

A joker in the pack for all bulk energy commodities will be the tariff on Chinese-built vessels, which could add up to US$30 for freight and would create a new dual freight market.

The API2 FQ25/front-quarter (FQ) “new” contract rose by four per cent MoM to US$100, within the short-term range of US$95-105. The Cal26 contract was up by four per cent to US$107. Brannvoll forecasts a range of US$100-130 and an average of US$125 for the FQ contract.

The API4 FQ contract fell three per cent to US$89, temporarily in a low range of US$90 -105. Brannvoll ApS maintains the forecast range of US$100-130 in 2025 for API2.

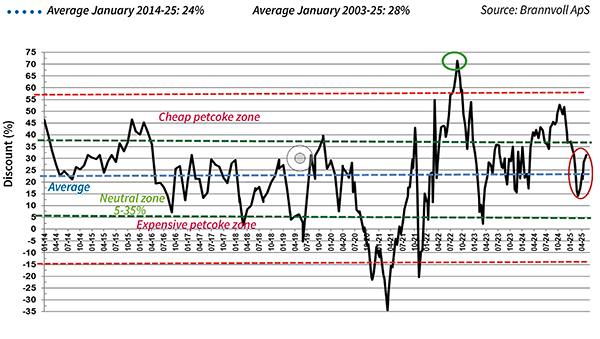

Petcoke

As forecast, the petcoke market has been reacting downwards. Very low discounts have led to cement producers and other users switching fast towards coal, with Russian and Colombian coal sellers seeing increased demand. Chinese and Indian buyers, busy in February, have stepped away from the markets, prompting traders long on high levels to lower prices.

The indications are that Indian buyers have switched to US NAPP and Australian coal. The potential introduction of disruption to the freight market, with Chinese built ships potentially impacted by tariffs, also deters spot business.

Depressed coal prices keep both FOB and ARA discounts so low that petcoke remains expensive unless it drops further. The USGC FOB 6.5 per cent sulphur (S) contract was down by five per cent MoM to US$80 and the discount unchanged to API4 at 28 per cent. The USGC ARA 6.5 per cent contract fell four per cent MoM to US$98.50, but the discount was rising from 14 to 21 per cent.

The USGC FOB 4.5 per cent S contract was down by two per cent MoM to US$88, with the FOB discount to API4 falling to 21 per cent. The CFR ARA 4.5 per cent contract declined two per cent to US$106.50, with the discount rising to 15 per cent due to a higher coal price.

by Frank O. Brannvoll, Brannvoll ApS, Denmark