Geopolitics and trade tariffs dominated the news during May and June. The suspension of the USA-China tariff battle should provide relief for at least a few months, raising the hope that other tariffs discussions will reach agreement.

Less positive has been the Ukraine–Russia conflict, with increased attacks from both sides despite US pressure for the two parties to negotiate a ceasefire. The Volatility Index (VIX) fell sharply from 60 to 17, signalling financial markets calming again, but how long will it last?

As was anticipated, the ECB lowered its interest rate again by 0.25 per cent to 2.00 per cent, while the Federal Reserve rate was unchanged, awaiting impact from the tariffs and the risk of new inflation.

The US dollar has been steady on the broad US$ index but was slightly lower against the euro falling to US$1.1420, indicating a range of US$1.12-1.16. Brannvoll ApS maintains its forecast range at US$1.05-1.15 in 2025, with an average of US$1.12.

| PRICES AT A GLANCE - 10 June 2025 | ||

| Brent crude oil – bbl | US$67.00 | |

| Coal API 2 | 3Q25 | US$100.00 |

| Cal 2025 | US$105.00 | |

| Coal API 4 | 3Q25 | US$91.00 |

| Cal 2025 | US$102.00 | |

| Petcoke USGC 4.5 per cent S 40HGI | FOB | US$70.50 |

| CFR ARA | US$89.00 | |

| Petcoke USGC 6.5 per cent S 40HGI | FOB | US$66.00 |

| CFR ARA | US$84.50 | |

Oil

Oil has recovered despite higher OPEC+ production, with some relief in the markets after China and the US started to talk. The risk of sanctions towards Iran and Venezuela also underpinned the market slightly.

For the third month, OPEC+ countries are not making any attempt to curb production, with US production flat and demand seeming to increase slightly.

The market outlook for the next few months will depend on how trade talks proceed, the outcome of USA-Iran negotiations and potentially new sanctions against Russia, should a peace settlement not be agreed with Ukraine.

TTF gas prices have been steady at around EUR35 (US$40.02) with warmer weather in Europe increasing demand for air conditioning and prompting the EU to replenish its stocks. Brannvoll ApS maintains a trading range of US$65-90 and average of US$75 for 2025.

Coal

The coal market remained very steady with no real news. Chinese and Indian production continues to increase, despite low demand from a weak Chinese property market, and very high stocks. Russian producers keep selling below production cost, with further closures of Russian and Australian mines expected. Colombian exporters have also lowered their output sharply as prices are too low. Expect the main indexes to remain in a narrow range.

The API2 FQ25/front-quarter (FQ) contract remained unchanged MoM at US$100, within the short-term range of US$95-105. The Cal26 contract was down by two per cent to US$105. Brannvoll forecasts a range of US$100-130 and an average of US$125 for the FQ contract.

API4 FQ contracts rose two per cent to US$91 temporarily in a low range of US$90 -105. Brannvoll ApS lowers the forecast range to US$100-130 in 2025 for API2.

Petcoke

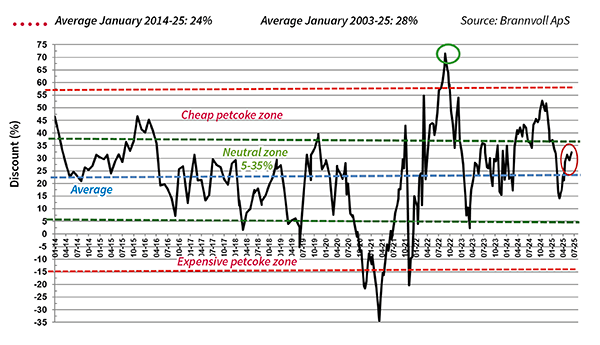

The petcoke market, which collapsed during the tariffs dispute between the USA and China, has remained weak, albeit rising up slightly from the lows. Chinese cement demand remains depressed due to the weak property market and India has also remained quiet in the high sulphur market.

Higher production in the USA is expected during June and July, adding further to a bleak outlook in the short term. Discounts have been recovering lately as the petcoke fell and coal remained steady.

The spread between 4.5 per cent and 6.5 per cent has decreased and Turkish buyers in particular have been looking for cheap mid-market petcoke, and the spread has been as low as US$2.

FOB and ARA discounts have increased and will likely lure buyers back to petcoke, but the tariff uncertainty and its impact on demand is keeping any aggressive purchasing at bay.

A ‘good solution’ between the USA and China will be balanced by higher US production in the near term. Risk is still to the downside depending on trade talks.

The UGC FOB 6.5 per cent sulphur (S) contract was down by two per cent MoM to US$66 and the discount to API4 at 42 per cent. The USGC ARA 6.5 per cent contract is up 0.5 per cent MoM at US$84.50, the discount up to 38 per cent.

The USGC FOB 4.5 per cent S contract was down by three per cent MoM to US$70.50, with the FOB discount to API4 up at 38 per cent. The CFR ARA 4.5 per cent contract was unchanged at US$89.00, with the discount rising to 29 per cent.

by Frank O. Brannvoll, Brannvoll ApS, Denmark