Geopolitics and tariff deals or negotiations are setting the tone for the energy complex.

The EU and USA have signed a deal with a 15 per cent tariff on EU exports but a 50 per cent tariffs on steel and aluminium as well as a pledge to purchase US energy products in the coming years. Tariff deals have also been reached with Japan and other individual countries. However, details and specifics are still largely missing, raising several questions for the impact on the markets.

Elsewhere, a ceasefire between Ukraine and Russia is being discussed at the time of writing, with the US deadline for an agreement approaching. The US is also threatening sanctions on countries buying Russian oil with discount, notably India and China. The conflict in the Middle East seems to have been contained and has been less of a concern for the markets.

Renewed risk of higher inflation and a potential recession in the USA, triggered by tariffs, is dampening demand in the energy markets and little likelihood of lower US interest rates, which has strengthened the US dollar. The central banks did not change rates in August as they await the tariffs outcome and monitor their impact on inflation.

The US dollar fell in the broad US$ index and towards the euro at US$1.16, still in the range of US$1.15-1.20. Brannvoll ApS forecasts a range of US$1.05-1.20 in 2025, with an average of US$1.12.

| PRICES AT A GLANCE - 6 August 2025 | ||

| Brent crude oil – bbl | US$67.00 | |

| Coal API 2 | 4Q25 | US$106.00 |

| Cal 2026 | US$111.00 | |

| Coal API 4 | 4Q25 | US$97.00 |

| Cal 2026 | US$102.00 | |

| Petcoke USGC 4.5 per cent S 40HGI | FOB | US$70.00 |

| CFR ARA | US$93.00 | |

| Petcoke USGC 6.5 per cent S 40HGI | FOB | US$66.00 |

| CFR ARA | US$89.00 | |

Oil

Oil has traded in a narrow range of US$67-72, driven by geopolitics. OPEC+ again increased its output in August and has now lowered its production cuts by 2.5mb/d to gain market share.

The market outlook for the coming months will depend how tariff talks proceed and the likelihood for a recession in the USA is seen as higher. The possibility of a secondary fee of 100 per cent on buyers of discounted Russian oil could lead to upward pressure on prices if Russian oil should need to be avoided due to the threat of tariffs, adding increased demand for OPEC+ and US oil.

TTF gas prices fell to EUR35 (US$41) and despite warm weather in Europe the EU gas storage has reached 70 per cent.

For Brent oil, Brannvoll ApS maintains a trading range of US$65-90 and average of US$75 for 2025.

Coal

The coal market slipped in July and August, reflecting lower oil prices and the slightly stronger US dollar.

India and China have seen somewhat lower demand due to floodings and monsoons, and the EU has replenished its coal storage during the month.

Trading has been low and there is no specific coal news, although China has introduced safety inspections that could lower domestic production and lead to an increase in Chinese prices. India has asked to lower domestic production due to high storage.

The API2 FQ25/front-quarter (FQ) contract fell three per cent MoM at US$106, still in short-term range of US$100-115. The Cal26 contract fell three per cent to US$111. Brannvoll forecasts a range of US$100-130 and an average of US$125 for the FQ contract.

API4 FQ25 contracts lost one per cent, down to US$97, staying in US$ short term range of US$95-105. Brannvoll ApS forecasts a range to US$100-125 in 2025 for API4.

Petcoke

The petcoke market saw very limited trading in July, as traders are assessing the new tariffs between the USA and China. After adding 40 per cent import tariffs on high-sulphur petcoke from 1 August, China has seen its imports from the USA come to a hold. The trading now needs to find new end users and suppliers, and has kept the market in a narrow range.

India is expected to come back to the market post monsoon. The market maintained a very narrow spread to US$3-4 between 4.5 and 6.5 per cent sulphur types.

Demand is low in Türkiye, and competes with cheap coal and domestic suppliers.

FOB discounts have increased slightly to lure buyers back to petcoke, but the tariff uncertainty and discounted Russian coal weighs on demand.

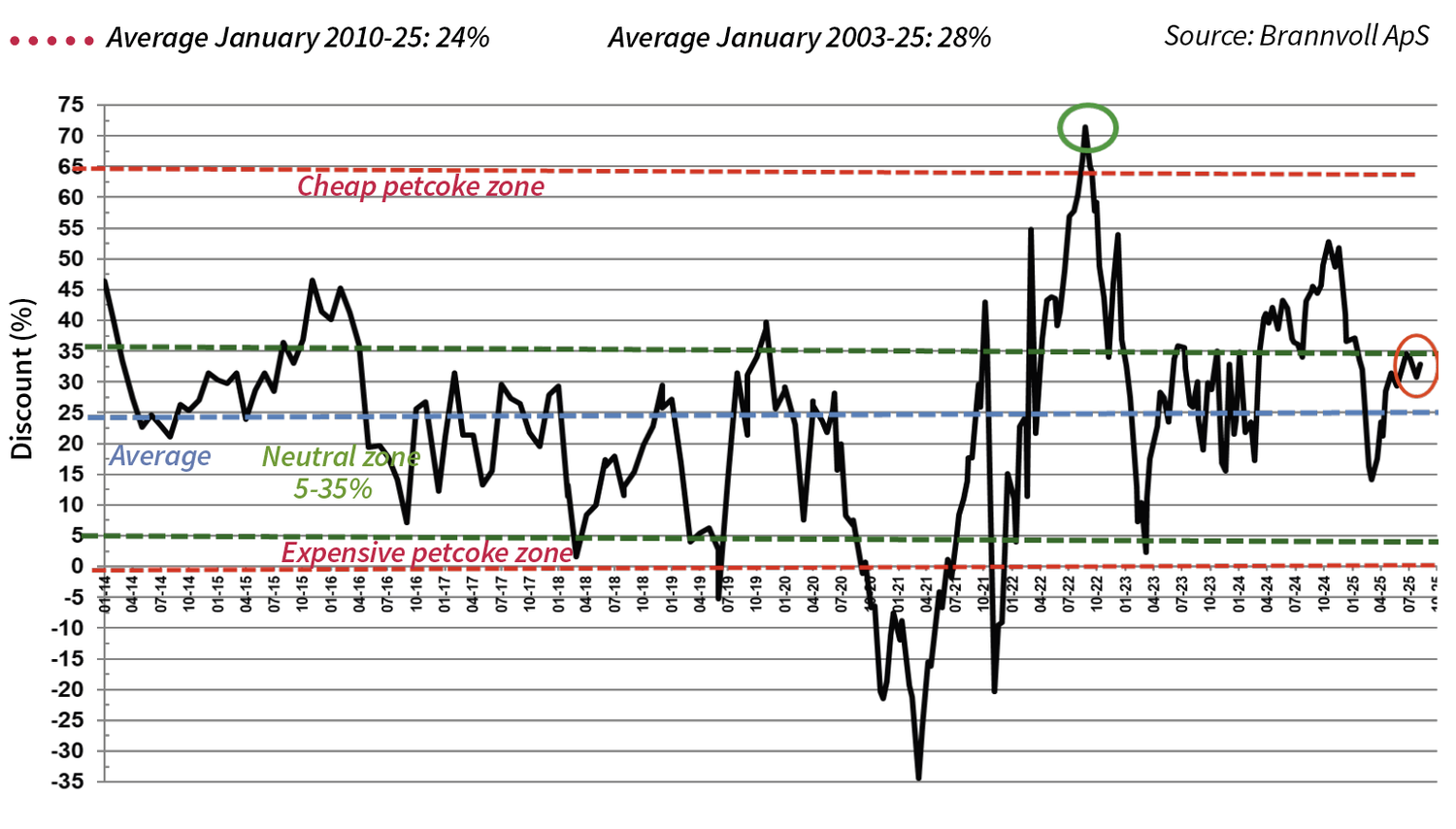

The USGC FOB 6.5 per cent sulphur (S) contract was down by three per cent MoM to US$66 and the discount to API4 at 46 per cent. The USGC ARA 6.5 per cent contract is down one per cent MoM at US$89, the discount down to 33 per cent due to lower API2.

The USGC FOB 4.5 per cent S contract was down by one per cent MoM to US$70, with the FOB discount to API4 at 42 per cent. The CFR ARA 4.5 per cent contract unchanged at US$93, with the discount at 30 per cent.