By Frank O. Brannvoll, Brannvoll ApS, Denmark

The energy complex fell in November, with oil leading the way. The Israel-Gaza war continued but still without any contagion – and no war premium. Ukraine-Russia war is frozen literally, and some hints of possible talks are emerging to the upcoming Russian election.

The US Federal Reserve and European Central Bank have both hinted in speeches that interest rates need to be high but not higher, which has given a relief rally in the financial markets. Both central banks are likely to consider easing interest rates when inflation is down to two per cent. The Chinese GDP continues to disappoint, lowering demand expectations in the energy markets.

The euro-US dollar went higher towards 1.09 but remains in its range of US$1.05-1.09.Brannvoll ApS maintains a range of US$1.00-1.15, with an average of US$1.10 in 2024.

|

Table 1: Prices at a glance – 4 December 2023 |

||

|

Crude oil (US$/bbl) |

78.00 |

|

|

Coal |

API2 – 1Q24 (US$) |

110.00 |

|

API2 – Cal 2024 (US$) |

109.00 |

|

|

API4 – 1Q24 (US$) |

108.00 |

|

|

API4 – Cal 2024 (US$) |

110.00 |

|

|

Petcoke |

USGC 4.5% 40 HGI – FOB (US$) |

72.00 |

|

USGC 4.5% 40 HGI – CFR ARA (US$) |

101.50 |

|

|

USGC 6.5% 40 HGI – FOB (US$) |

65.50 |

|

|

USGC 6.5% 40 HGI – CFR ARA (US$) |

95.00 |

|

Oil

Despite the ongoing geopolitical problems, including threat of war in South America with Venezuela looking to annex a large share of Guyana’s oil-richest land, the oil price continued to slide below the psychological barrier of US$80. This prompted the OPEC+ countries to initiate further cuts. The cuts now total 2.2mb/d, including Saudi Arabia’s 1mb/d, Russia’s current 0.3mb/d cuts and a 0.9mb/d reduction voluntarily distributed among the OPEC members. Russia is pledging 0.2mb/d of additional cuts. OPEC also announced that Brazil will join the organisation from 2024. The market did not respond positively, with prices at the time of writing below US$80. Iran used a price of US$71 in its 2024 budget.

In addition, Venezuela will increasingly be supplying oil for export while the USA is seeing production at record levels. However, OPEC has pledged to do “whatever is necessary” so the game is not over yet. For now, the short-term range is set at US$75-85 with geopolitics being the joker among new OPECs initiatives. Brannvoll ApS forecasts a trading range US$80-110/bbl, with an average of US$95/bbl for 2024.

Coal

Coal prices again retraced with oil and lower Chinese domestic prices. ARA stocks edged up, but demand from Europe has faded dramatically. Some support was seen as German coal producers want to keep a coal-fired back-up in place despite a temporary permit running out in 2024.

China is buying again from Australia while Russia continues its policy of discounted sales but is seeing some problems following an export terminal fire and the introduction of a Russian export tax. Meanwhile, the COP 28 does not seem to have any major impact on the markets.

The API2 front-quarter (FQ) contract fell by one per cent MoM to US$111, maintaining a short-term range of US$105-125. The API2 Cal24 contract slipped one per cent MoM to US$114.50. Brannvoll ApS forecasts a range of US$100-135 and average of US$125 for both 1Q24 and Cal24 contracts with the Cal24 ranging between US$100-130.

The API4 FQ contract surprised the markets with a nine per cent MoM drop to US$108, lowering the short-term range of US$105-120. The API4 Cal24 contract was also down nine per cent MoM to US$110. Brannvoll ApS expects a range US$100-150 in 2024 as volatility is higher in API4.

Petcoke

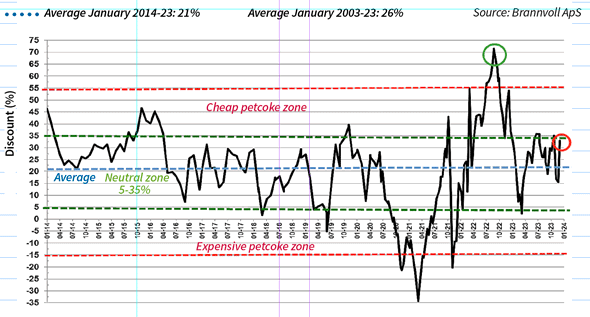

The big drop happened in petcoke which was literally dumped during November for December deliveries, with prices down four weeks in a row as buyers were very reluctant to take in material by year-end. Moreover, following the lifting of sanctions, Venezuela, with massive petcoke surplus stocks, is more active in the mid-sulphur market. The October rally turned to a crash that lifted discounts from expensive to cheap petcoke. The lower oil gas and especially coal prices scared buyers away with “panic before closing” by the traders who were caught long. The market has now reached major support levels in the US$60s and switching could take up the start of the new financial year. In Turkey the competition with Russian coal remains, but Venezuelan exports are emerging.

Petcoke discount to coal – API2 USGC 6.5% USGC ARA based on 6000kcal: Dec 2023: 33%

The USGC FOB 6.5 per cent sulphur (S) contract collapsed 30 per cent MoM to US$65.50 while the discount to API4 shot up to 51 per cent. The USGC ARA 6.5 per cent S contract was down only 18 per cent MoM to US$95 and discount up to 33 per cent. This was due to sharply increased ARA rates.

The USGC FOB 4.5 per cent S contract dived 29 per cent MoM at US$172, with the discount to API4 up to 47 per cent. The CFR ARA 4.5 per cent contract fell by 17 per cent MoM to US$101.5 with the discount higher to 27 per cent.

At these levels petcoke is in the cheap zone, which is often short-lived, and unless coal drops below US$100, it could be a buying opportunity.