It has been another month dominated by geopolitics, most prominently the conflict between Israel and Iran. The bombing and missile exchanges led to a jump in oil prices before it became clear that Iran would close the Strait of Hormuz, being dependent on its own exports to China and India. At the time of writing, it seems the declared ceasefire is being respected by both Israel and Iran.

Meanwhile, the conflict in Gaza also seems to be advancing towards a ceasefire, based on US-led peace proposals. Less optimistic is the Ukraine-Russia conflict with new attacks from both sides and the markets wondering whether the next US move of reducing weapon deliveries may impact upon Ukraine’s willingness to discuss a peace plan.

The central banks did not change rates over the last months and will likely await the outcome of tariffs talks and monitor the impact on inflation which both in the USA (2.4 per cent) and the euro area (2.0 per cent) are back at acceptable levels. The US dollar fell against the broad US$ index and towards the euro at US$1.18 and is now adjusting range to US$1.15-1.20. Brannvoll ApS forecasts in the range of US$1.05-1.20 in 2025, with an average of US$1.12.

| PRICES AT A GLANCE - 3 July 2025 | ||

| Brent crude oil – bbl | US$68.00 | |

| Coal API 2 | 3Q25 | US$109.00 |

| Cal 2025 | US$114.00 | |

| Coal API 4 | 3Q25 | US$99.00 |

| Cal 2025 | US$107.00 | |

| Petcoke USGC 4.5 per cent S 40HGI | FOB | US$71.00 |

| CFR ARA | US$93.00 | |

| Petcoke USGC 6.5 per cent S 40HGI | FOB | US$68.00 |

| CFR ARA | US$90.00 | |

Oil

Oil experienced a substantial rally from US$65 to US$80 based on Israel’s attack on Iranian nuclear facilities. However, as soon as the market realised supply would remain it retraced to US$66. Subsequently, OPEC+ decided to add more supply to the markets and prices are back in the US$65-70 range.

The market outlook for the next few months will depend how tariffs talks will proceed and if the Israel-Iran ceasefire holds, with no closing of Hormuz. The conditions of the Iranian nuclear facilities will also play a factor as further attacks cannot be ruled out in the near future, underpinning nervousness in the oil market.

TTF gas prices rose to EUR40 (US$47), with warmer weather in Europe increasing demand for cooling and for the EU to replenish its stocks. However, this also fell back towards EUR35. Brannvoll ApS maintains a trading range of US$65-90 and average of US$75 for 2025.

Coal

The coal market rose during June and July, driven up by oil, a lower US dollar and European cooling demand, as nuclear reactors were having less cooling water and running with lower capacities in France. There is no real coal news. Colombia is seeing exports fall. Russian traders are still selling on discount to markets without sanctions setting a lid on any price spikes. The lower US dollar and higher gas prices underpinned the market in the short term. China and India have very large stocks and both countries’ domestic production has increased, lowering demand for import. The main indexes are now close to expected upper levels.

The API2 FQ25/front-quarter (FQ) contract rose nine per cent MoM to US$109, within the short-term range of US$100-115. The Cal26 contract added nine per cent rising to US$114. Brannvoll forecasts a range of US$100-130 and an average of US$125 for the FQ contract.

API4 FQ contracts added seven per cent, up to US$98, back close to US$ range of US$95 -105. Brannvoll ApS lowers the forecast range to US$100-125 in 2025 for API4.

Petcoke

The petcoke market remained calm even with higher coal prices, with very few deals as traders are fearful of tariffs and the impact on demand.

The market has seen a significant shift towards more production of medium sulphur and less high sulphur types due to lighter crude oil used. This has led to a narrowing of the spread between 4.5 per cent and 6.5 per cent sulphur to US$3.

Demand remains weak in Türkiye and China as well as India due to monsoons, while high stocks in China accounts for moderate price moves and increased discount.

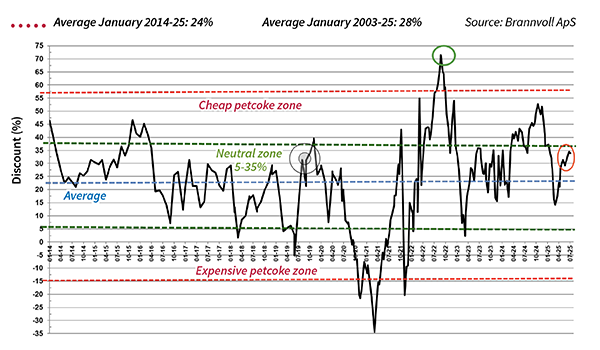

FOB and ARA discounts have increased and will lure buyers back to petcoke, but the tariffs uncertainty and cheap Russian coal weigh on demand.

The USGC FOB 4.5 per cent S contract was up by 0.5 per cent MoM to US$71, with the FOB discount to API4 up at 43 per cent. The CFR ARA 4.5 per cent contract was up four per cent at US$93, with the discount at to 32 per cent.

The UGC FOB 6.5 per cent sulphur (S) contract was up by two per cent MoM to US$68 and the discount to API4 at 45 per cent. The USGC ARA 6.5 per cent contract was up 6.5 per cent MoM at US$90, the discount down to 38 per cent.

by Frank O. Brannvoll, Brannvoll ApS, Denmark