By Frank O. Brannvoll, Brannvoll ApS, Denmark

The same geopolitical factors as last month are dominating the energy markets. The persistently-high inflation is driving the agendas of the central banks with higher interest rates, stating they will push even harder despite a looming recession. As industry and citizens save energy due to the high prices, demand in many markets is contracting sharply. Politicians are trying to introduce different measures in the EU to curb prices with windfall taxes, but these are very difficult to implement.

The sabotage of Gazprom’s North Stream 1 and 2 gas pipelines in the Baltic Sea only lifted the market a little, underlining the bearish tone. It is expected that it would take at least two months to repair the leaks. Even if sanctions are lifted, gas would not be able to flow from Russia.

In October-November we will see how industry will cope with new hedging in 2023 or further reduce production.

The situation in Ukraine may also be coming into a final phase after the “referendums”, showing the potential for a peace deal that both parties could live with.

The US dollar has risen sharply on the overall US$ Index , forcing US$-denominated commodity prices lower. The euro fell again to US$0.98 and is seen on a lower range of US$0.95- 1.05 as long as the ECB lags FED on interest rate hikes.

|

Prices at a glance |

|

| Crude oil - bbl | US$98.50 |

| Coal API2 - 4Q22 | US$255.00 |

| - Cal2023 | US$240.00 |

| Coal API4 - 4Q22 | US$250.00 |

| - Cal2023 | US$238.00 |

| Petcoke - USGC 4.5% 40HGI FOB | US$148.00 |

| CFR ARA |

US$173.00 |

| Petcoke - USGC 6.5% 40HGI FOB | US$138.00 |

| CFR ARA | US$163.00 |

Oil and gas

Oil fell to US$83 and on 5 October OPEC+ decided to cut production with 2mbpd – underlining the new central role to defend oil price around US$90. Brent rose sharply to US$98 but is still trapped by a stronger US$ and the general slowdown in demand.

Awaiting new Chinese growth packages, the World Bank cut growth of the world’s largest consumer, China.

The oil price is seen in a wide range of US$85-115 driven by geopolitics, recession fears and with OPEC watching.

Coal

Coal finally followed the overall energy complex downwards. Europe has been buying erratically to secure fuel stocks for the winter as coal was by far cheapest fuel. Different logistical issues in the export countries kept prices high. ARA stocks are now at an historic high, and the buying spree has dampened amid lower power demand due to the extreme prices and general fall in industrial demand.

Russia has continued selling coal with huge discounts, forcing other producers to lower prices to keep market shares in the countries not taking part of the EU-US sanctions against Russia. The fall of many emerging market currencies to the US dollar has also pushed the coal price downwards. Gas and EUA prices have also fallen, adding to the bearish sentiment.

The API2 front-quarter (4Q22) contract fell 22 per cent MoM to US$255 with a new lower range of US$220-300 expected. The API2 Cal23 contract fell 17 per cent MoM at US$240, pushing the forecast range downwards to US$210-290.

The API4 front-quarter (4Q22) contract fell 23 per cent MoM to US$250, into a lower range of US$220-290. The API4 Cal23 contract fell 16 per cent MoM to US$238, breaking the uptrend and a new lower range of US$295-340 range.

Petcoke

As predicted petcoke has been seen as the cheap fuel, with record-high discounts to coal. Indian and Chinese buyers have looked for supply, bidding up prices. In China the glassmakers have eased the sulphur requirements, giving new demand for higher sulphur products. Some distortions in the USGC refineries slightly lowered output, underscored by a fall in capacity utilisation.

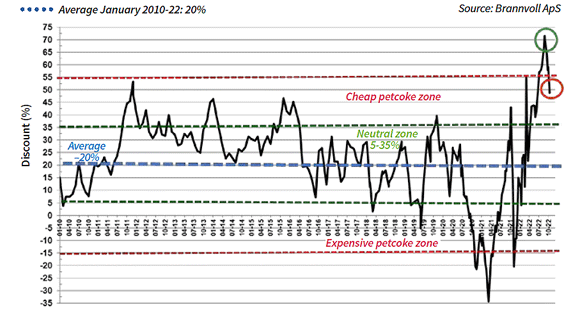

Petcoke discount to coal – (API2 USGC 6.5% USGC ARA based on 6000kcal) Nov 2022: 49%

As petcoke was cheap compared to even Russian discounted coal, new buyers were active in the markets. Venezuelan exports are rising to China and Turkey, where potential sanctions from the US are not seen in terms of petcoke. European buyers are still reluctant and are facing potentially lower cement demand in 2023, but with coal prices still high, many will start purchasing petcoke if production is to continue. As forecast, discounts have started to fall as coal prices declined and petcoke prices increased.

The USGC FOB 6.5 per cent S contract is up 10 per cent MoM at US$138, with the discount to API4 reduced to 56 per cent. The USGC CFR ARA 6.5 per cent contract is up 13 per cent per cent MoM to US$163 as a result of higher freight rates with the discount down from 65 to 49 per cent.

The USGC FOB 4.5 per cent S contract is up 14 per cent MoM at US$148, with the discount to API4 down to 53 per cent. The CFR ARA 4.5 per cent contract is up 15 per cent MoM to US$173 due to higher freight rates, with the US$25 discount down to 46 per cent towards API2.