By Frank O. Brannvoll, Brannvoll ApS, Denmark

Another month with the European Central Bank (ECB) and the US Federal Reserve in focus: in the US the interest rate has been increased by 0.25 per cent while the ECB notched up the rate by 0.5 per cent. However, inflation seems stubbornly high. Therefore, it is expected that rates will increase further and remain high for some time with fears of a recession continuing albeit to a lesser degree. The IMF has adjusted global growth up by 0.2 per cent to 2.9 per cent in 2023, driven by growth in China and India.

In the energy markets, the G7 is introducing another round of sanctions on Russian refined products from the start of February. Overall the energy prices have seen a falling trend due to the mild winter in general and European consumers considerably cutting back consumption. Despite weapon deliveries and lots of talk, the frontlines in Ukraine seem frozen, and rumours are that a “realistic” settlement needs to be found soon for the benefit of all parties.

The euro reached US$1.10 and is now in a new range of US$1.05-1.10. It is not likely to appreciate further over the next months. For 2023 Brannvoll ApS expects the euro to move within a range of US$0.90-1.10, with an average of US$1.02.

| Prices at a glance | ||

| Brent crude oil (bbl) | US$79.80 | |

| Coal API2 |

1Q23 | US$141.00 |

| Cal 2023 |

US$150.00 | |

| Coal API4 |

1Q23 | US$146.00 |

| Cal 2023 |

US$138.00 | |

| Petcoke USGC |

4.5% 40HGI FOB |

US$149.00 |

| 4.5% CFR ARA |

US$165.50 | |

| 6.5% 40HGI FOB | US$137.00 | |

| 6.5% CFR ARA | US$153.00 | |

Oil and gas

OPEC+ held a 25 minute-long meeting and kept its target for 2mbpd production cuts. The markets are monitoring China reopening for large trends. The geopolitical situation remains tense with simmering tensions between China and the USA over Taiwan and the incident of the Chinese balloon, shot down by the US, adding to the ongoing war in Ukraine. The effect of new sanctions on Russian refined products such as diesel is still to be seen.

The oil market has seen stocks building in the US and in combination with fears over falling demand, this led to a volatile drop from US$89 to just below US$80, confirming the expected US$78-90 range in the coming month. The short-term range for Brent is expected to be US$75-88/bbl.

For 2023 Brannvoll ApS expects the oil price to move within a range of US$80-115/bbl, with an average of US$98/bbl.

Coal

Coal continued its dramatic fall from glory with a 70 per cent drop from highs last year putting pressure on gas and petcoke prices.

The supply disruptions have been resolved. Increased production in China, in combination with rebates from Russian coal sellers, maintains the negative pressure on the market. The impact from Australian imports into China is expected to be seen in the next quarters. Furthermore, Colombian rates are increasingly competitive and also pressure market prices. However, at the current coal price levels, buyers are urged to compare budget rates and look for buying opportunities.

The API2 front-quarter (2Q23) contract fell by 20 per cent MoM to US$141. The API2 Cal24 contract fell 12 per cent MoM at US$150. For 2023 Brannvoll ApS adjusts the range down to US$150-250 with an average of US$200 for the quarterly and calendar year API2 contracts.

The API4 front-quarter (2Q23) contract fell by 10 per cent MoM to US$149. Adjusting the forecast down, a range of US$150-250 is expected with an average of US$200 in 2023. The API4 Cal23 contract rose three per cent MoM to US$166. In 2023 the price is expected to range between US$150-280 with an average of US$200.

Petcoke

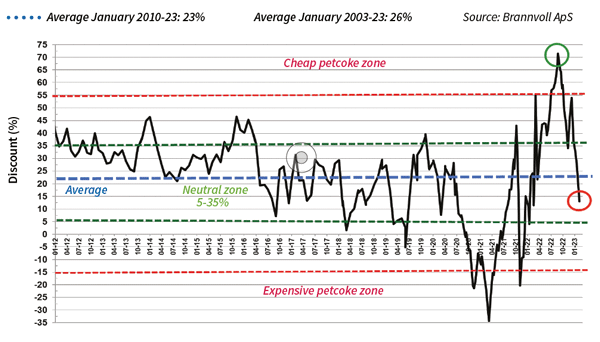

Petcoke prices rose despite the declining coal prices, based on very low supply and falling freight rates, which supported petcoke FOB prices. The capacity fall in the USGC as well as RIL, India, only producing to own gasification kept spot prices higher, but activity remained low. China is seen awaiting the impact from coal and more cement buyers are increasingly turning towards relatively cheap coal as the discounts now are in the ‘expensive zone’, a dramatic swing from the ‘very expensive zone’ just a few months ago when coal prices were twice the current quarter level.

Petcoke discount to coal – API2 USGC 6.5% USGC ARA based on 6000kcal: Feb 2023: 13%

The USGC FOB 6.5 per cent sulphur (S) contract is up eight per cent MoM to US$136, with the discount to API4 dropping from 39 to 25 per cent. The USGC CFR ARA 6.5 per cent S contract rose by three per cent MoM to US$153.50, as freight rates fell to US$16.50 and the discount dropping to 13 per cent and now moving into the expensive zone. The USGC FOB 4.5 per cent S contract rose eight per cent MoM at US$149, with the discount to API4 down to 18 per cent. The CFR ARA 4.5 per cent contract rose by three per cent MoM to US$165.50 with the discount toward API2 as low as nine per cent.