It has been another month dictated by geopolitics. The USA and China have agreed to extend tariffs implementation to 12 November to reach a mutual agreement. In Ukraine the war continues despite the Alaska summit and various plans are being discussed. The USA has said it will consider further sanctions against Russia – and the EU seems to be willing to keep the war going on – leaving Ukraine’s situation unresolved.

Despite new highs in equity markets the economic situation continues to look bleak, with inflation increasing and unemployment ticking up in the USA.

In the worst case this could lead to stagflation, which could hurt demand and trigger even higher interest rates. A lot of growth in the USA is currently bound towards AI and technology associated infrastructure such as data centres. In Europe the central bank has warned that interest rates may not go much lower, and in the US the Federal Reserve seems to move towards lowering rates in September with the markets expecting an increase of up to 0.5 per cent.

The US dollar fell in the broad US$ index and towards the euro at US$1.17, still in the range of US$1.15-1.20. Brannvoll ApS forecasts a range of US$1.05-1.20 in 2025, with an average of US$1.12.

| PRICES AT A GLANCE - 5 September 2025 | ||

| Brent crude oil – bbl | US$66.30 | |

| Coal API 2 | 4Q25 | US$97.00 |

| Cal 2026 | US$103.00 | |

| Coal API 4 | 4Q25 | US$92.00 |

| Cal 2026 | US$97.00 | |

| Petcoke USGC 4.5 per cent S 40HGI | FOB | US$70.00 |

| CFR ARA | US$97.00 | |

| Petcoke USGC 6.5 per cent S 40HGI | FOB | US$65.50 |

| CFR ARA | US$92.50 | |

Oil

Oil has continued trading in a very narrow range of US$65-69 driven by geopolitics and statements from OPEC+. OPEC+ has, as expected, raised its production but warned in August that further increases could be reduced due to weaker market demand, especially from China.

The impact on Russian oil from new sanctions, such as higher tariffs towards India for purchasing Russian oil, will also be a factor in the supply and demand.

Rebuilding of strategic reserves especially in China has been a supporting factor during July-August.

Brent oil is currently trading at US$66.30.TTF (Cal26) gas prices fell to EUR32.50 despite EU gas storage increasing from 70 to 79 per cent. For Brent oil, Brannvoll ApS maintains a trading range of US$65-90 and average of US$75 for 2025.

Coal

The coal market continued to slip in August, based on lower demand and good supply.

Colombian and Russian sellers have been offering good discounts, pushing the short- and medium-term prices lower.

India and China both have relatively large stocks at plants and in ports, and have taken advantage of discounts from Russia. ARA stocks have been low due to low water levels in the Rhein but are being replenished.

The API2 4Q25/front-quarter (FQ) contract fell eight per cent MoM to US$97, in the lower short-term range of US$95-110. The Cal26 contract fell seven per cent to US$103. Brannvoll forecasts a range of US$100-130 and an average of US$125 for the FQ contract.

API4 4Q25/FQ contracts lost five per cent, down to US$92 in lower, short-term range of US$90-100.

Brannvoll ApS forecasts a range of US$100-125 in 2025 for API4.

Petcoke

The petcoke market saw very narrow price range in August. Higher freight rates to key markets kept a lid on the FOB prices, while lower coal prices limite kept any potential upside.

India was back on the buy side after the monsoon, while Chinese traders may be returning after the extention to US tariff negotiations. However, Türkiye saw higher imports during July, including from Venezuela. Domestic production in Türkiye was also higher.

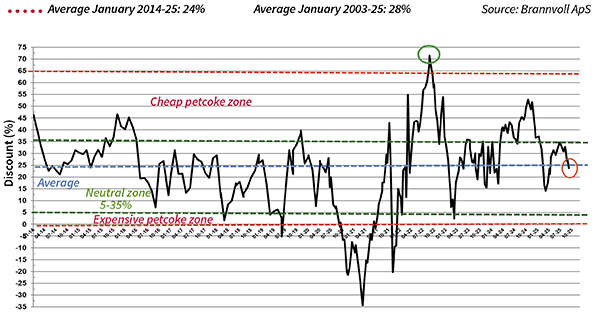

As US Gulf refiners increase imports of heavier crude oil, production of the 6.5 per cent sulphur (S) grade is expected to rise, while output of medium-sulphur grades is likely to decline. This will widen the spread between 4.5 and 6.5 per cent from the narrow range seen last quarter up from US$3 to US$4.5. The USGC FOB 6.5 per cent contract dropped one per cent MoM to US$65.50 and the discount to API4 fell to 43 per cent.

The USGC ARA 6.5 per cent contract is up four per cent MoM at US$92.50, the discount down to 24 per cent due to lower API2.

The USGC FOB 4.5 per cent S contract is unchanged MoM to US$70, with the FOB discount to API4 at 39 per cent. The CFR ARA 4.5 per cent contract was up four per cent at US$97, with the discount down at 20 per cent. The ARA moved higher due to a surge in freight rates.

By Frank O. Brannvoll, Brannvoll ApS, Denmark